The landscape of residential investment within the Greater Toronto Area (GTA) has entered a period of structural transformation as of early 2026. This transition is characterized by a definitive move away from speculative condominium acquisition toward the strategic densification of low-rise residential assets, a phenomenon frequently described in the industry as the return of the "missing middle". As traditional market drivers, such as high-velocity population growth and low interest rates, have reached a point of cyclical moderation, the emergence of as-of-right zoning for multiplexes and the implementation of sophisticated federal financing incentives have created a new paradigm for institutional and private wealth creation. The following analysis examines the economic, regulatory, and financial mechanisms currently shaping the GTA market and provides a strategic framework for the generation of investment-focused content tailored to the contemporary market participant.

The Macroeconomic Context and Segmented Market Performance

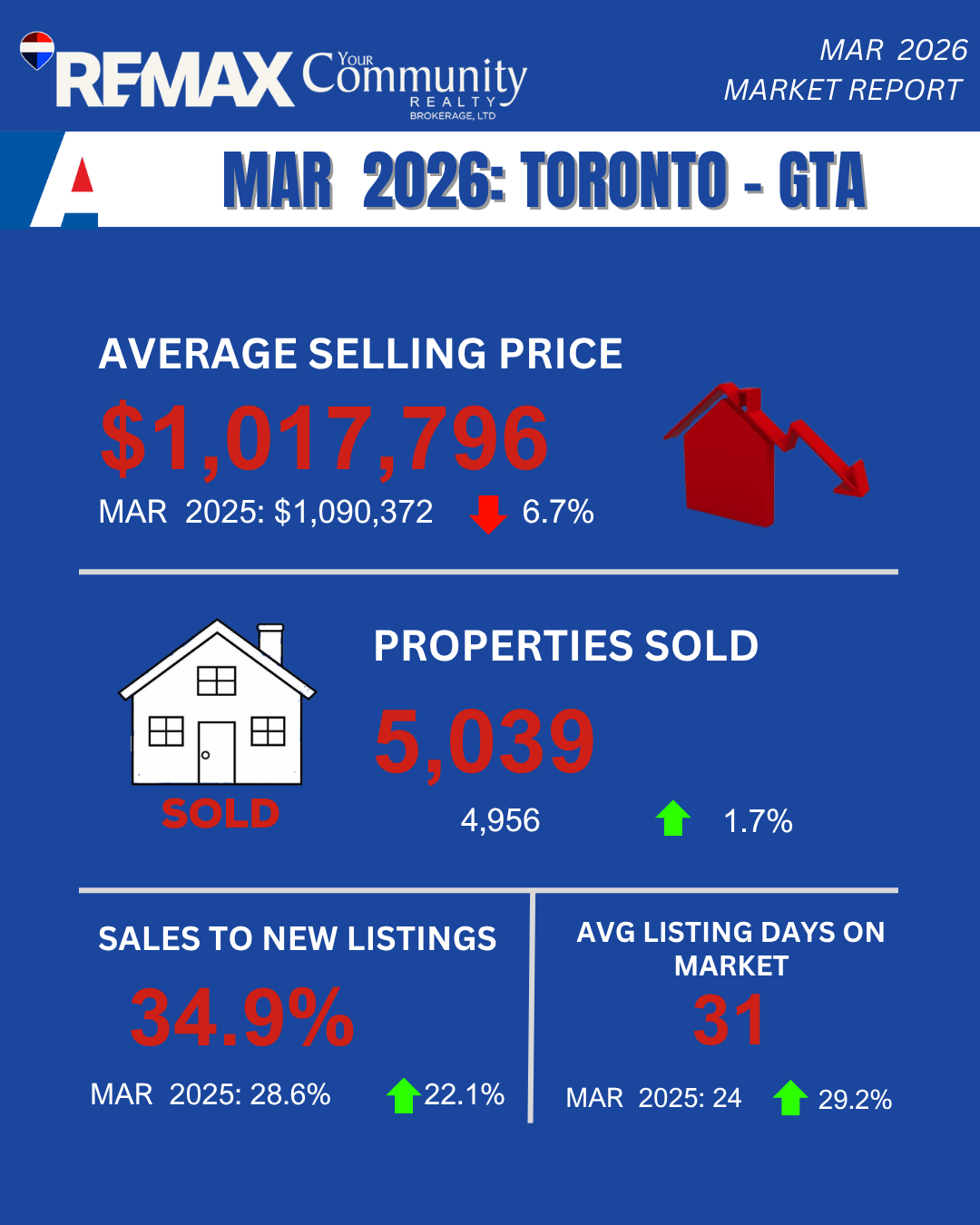

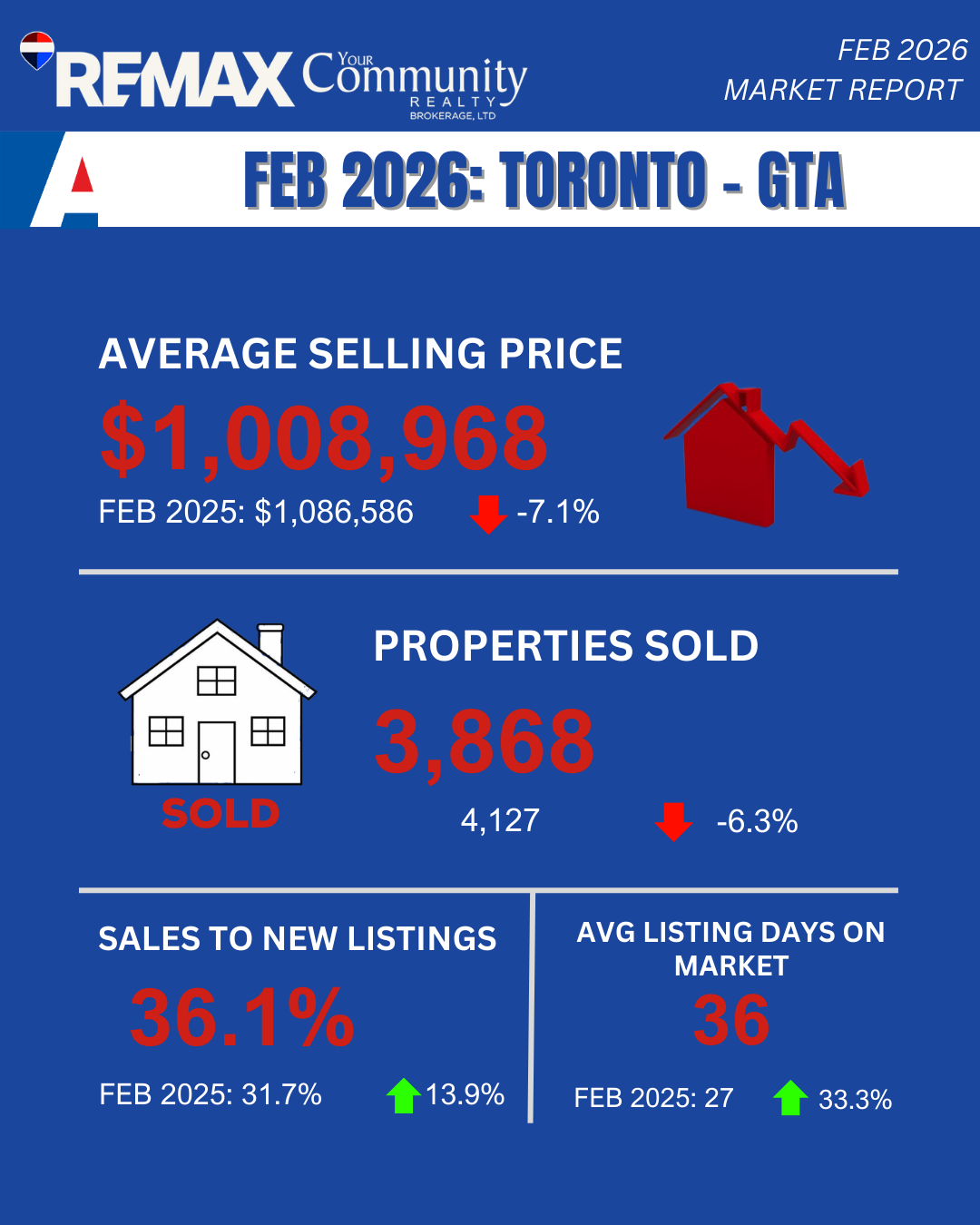

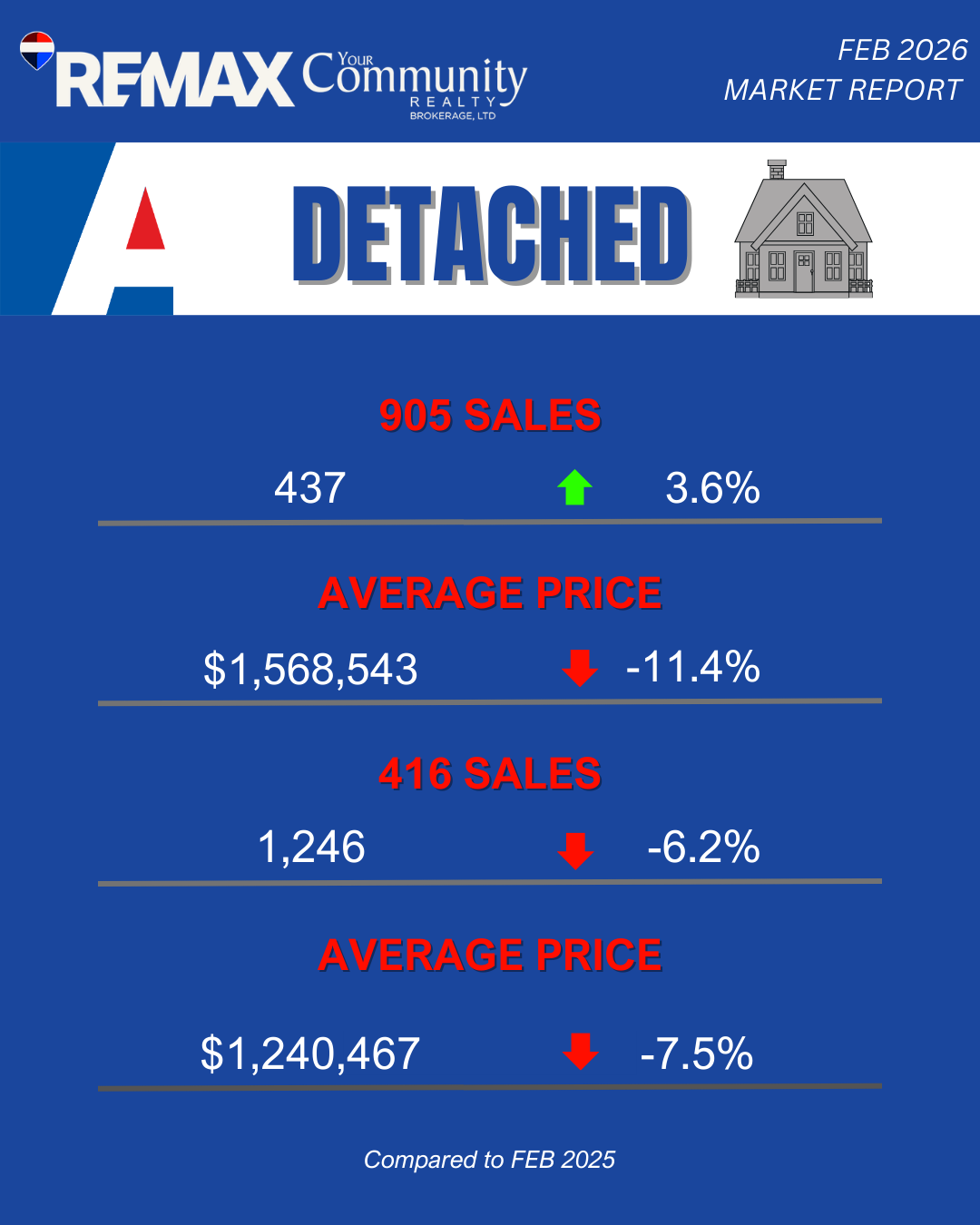

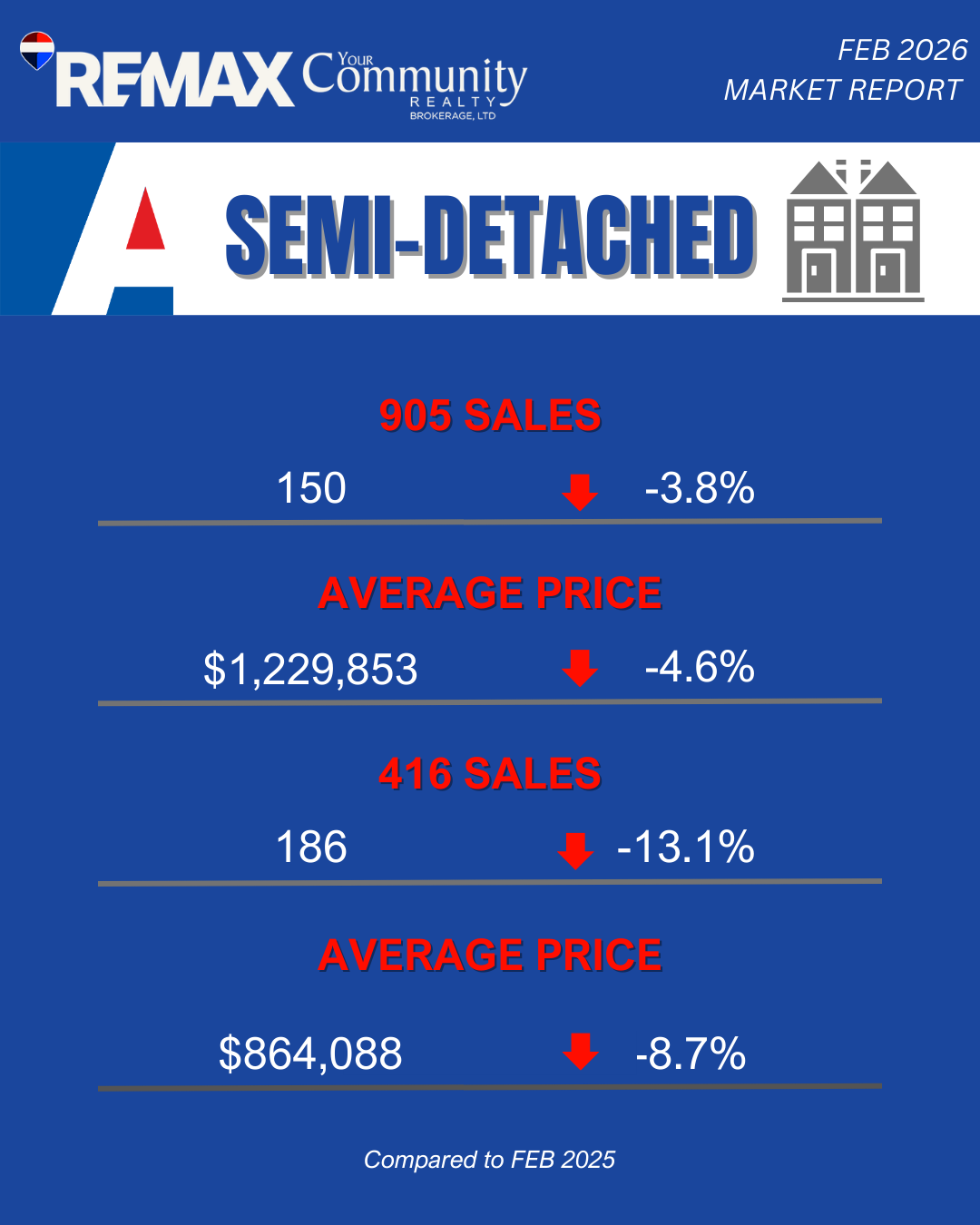

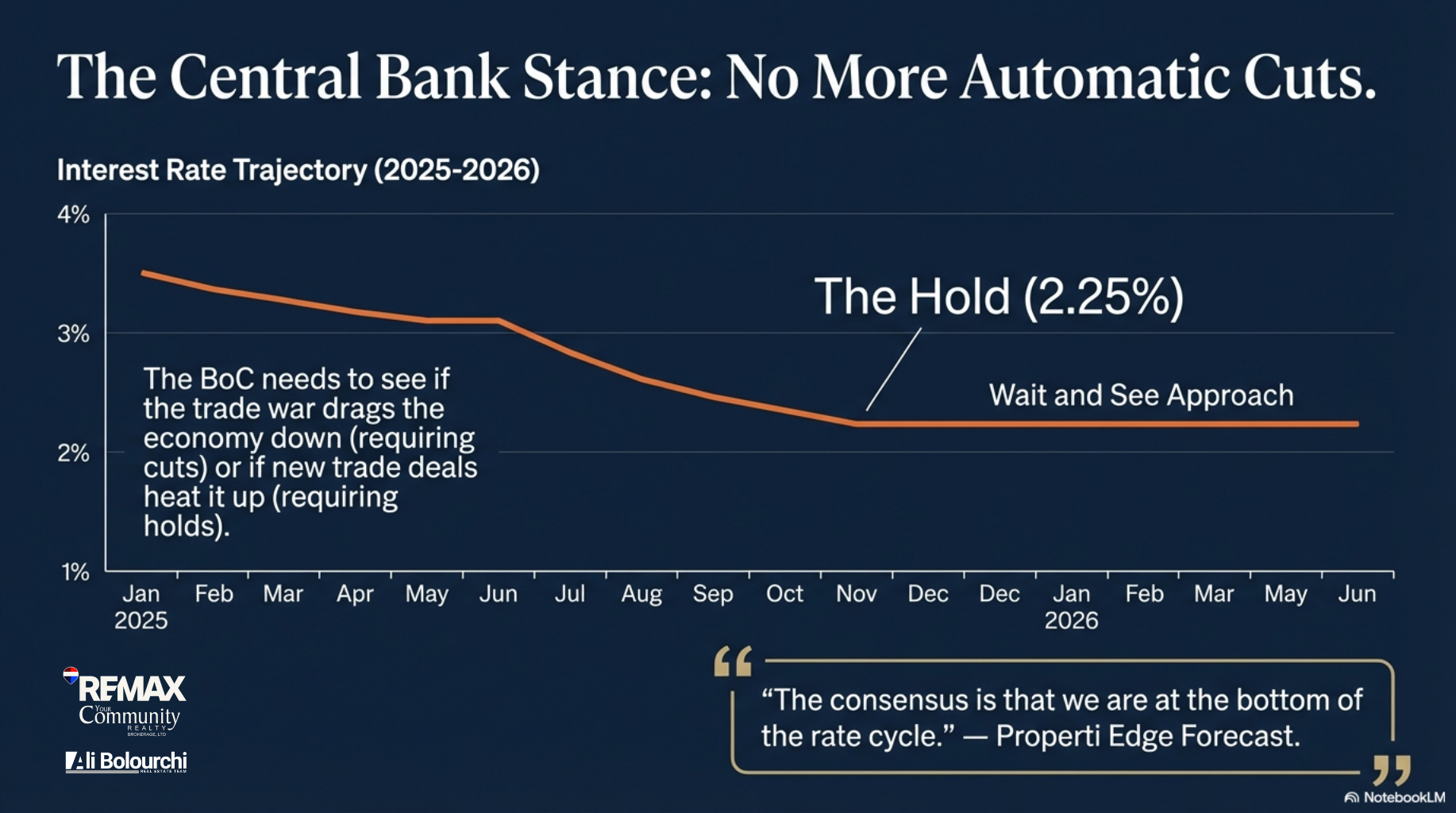

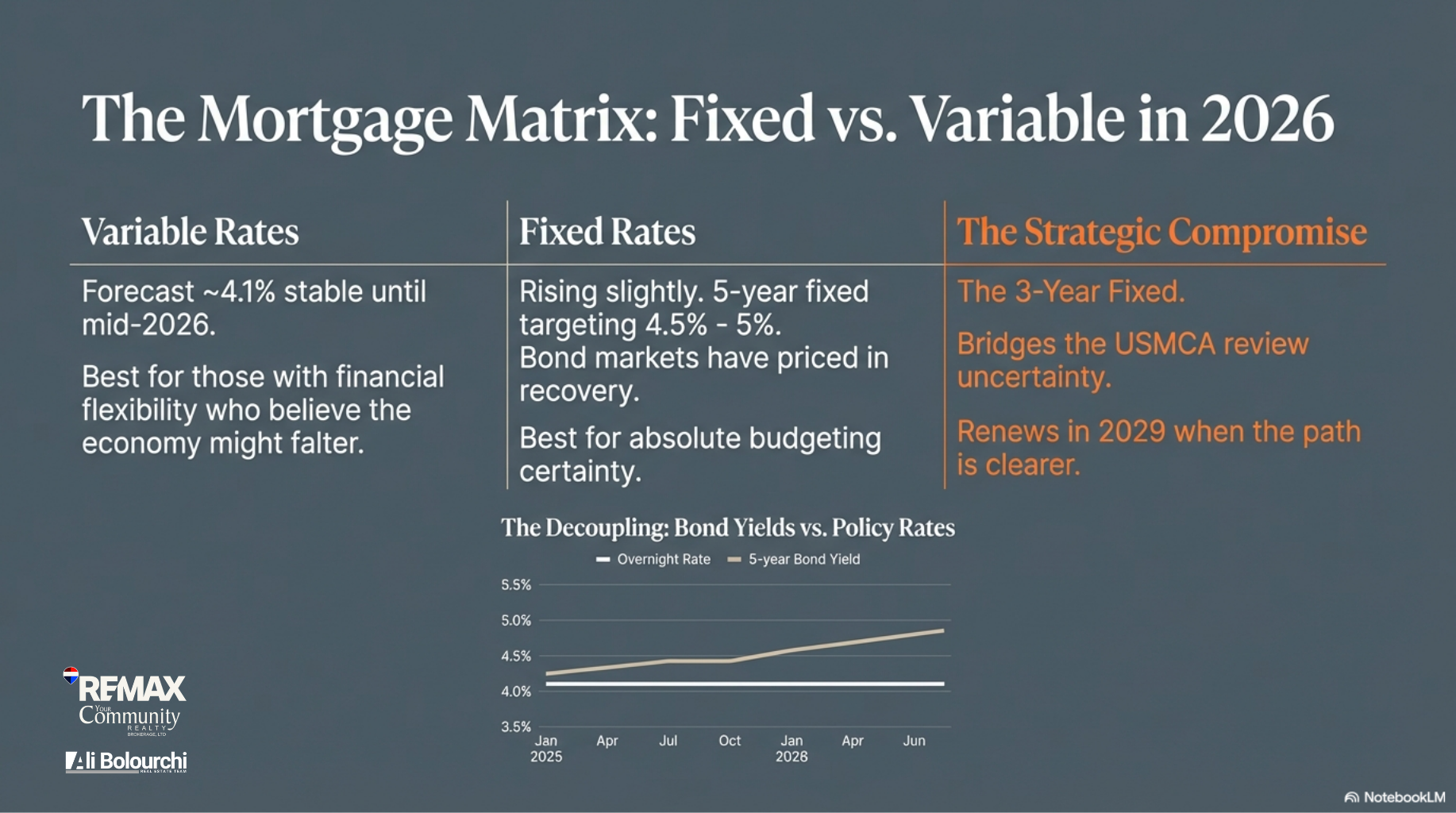

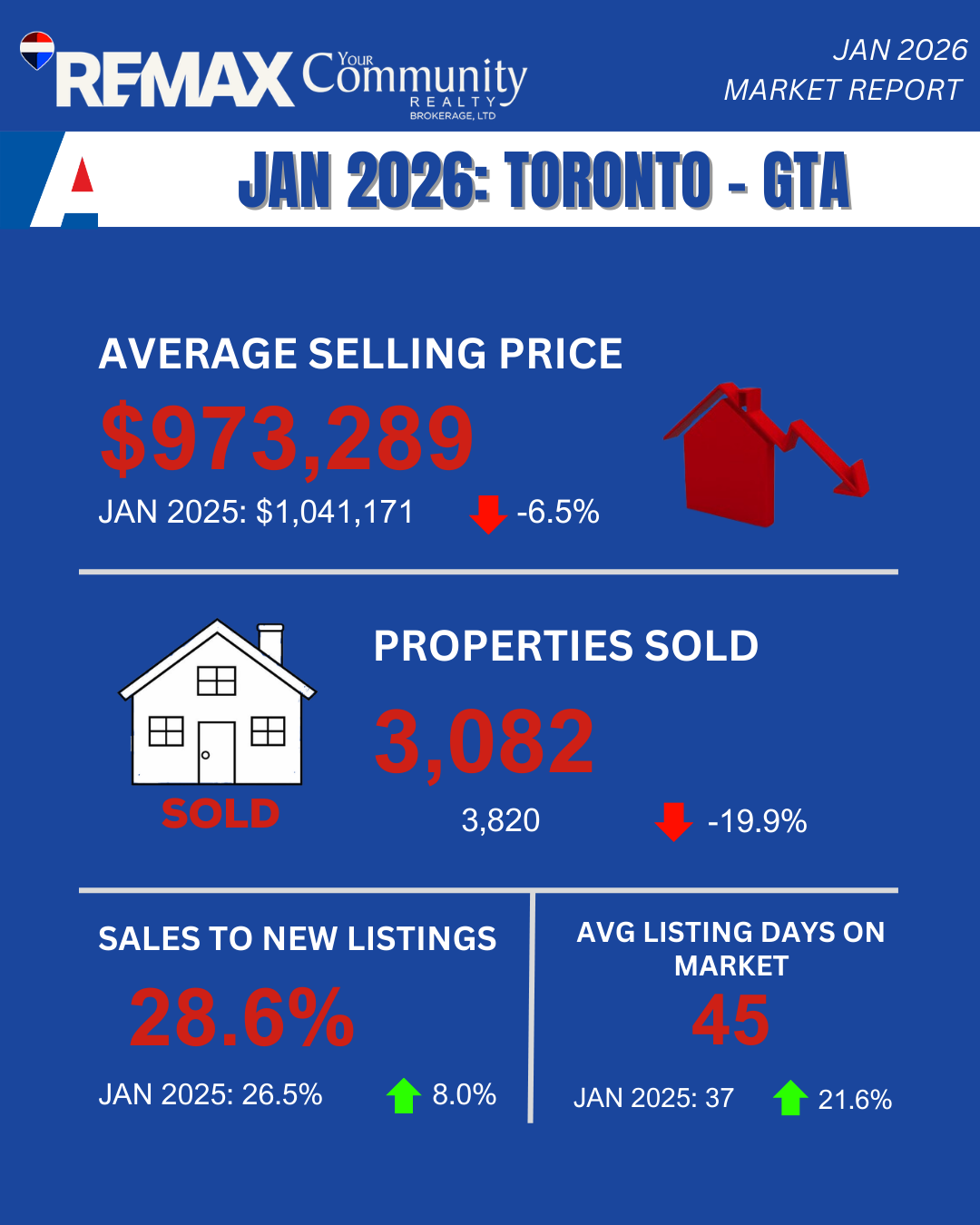

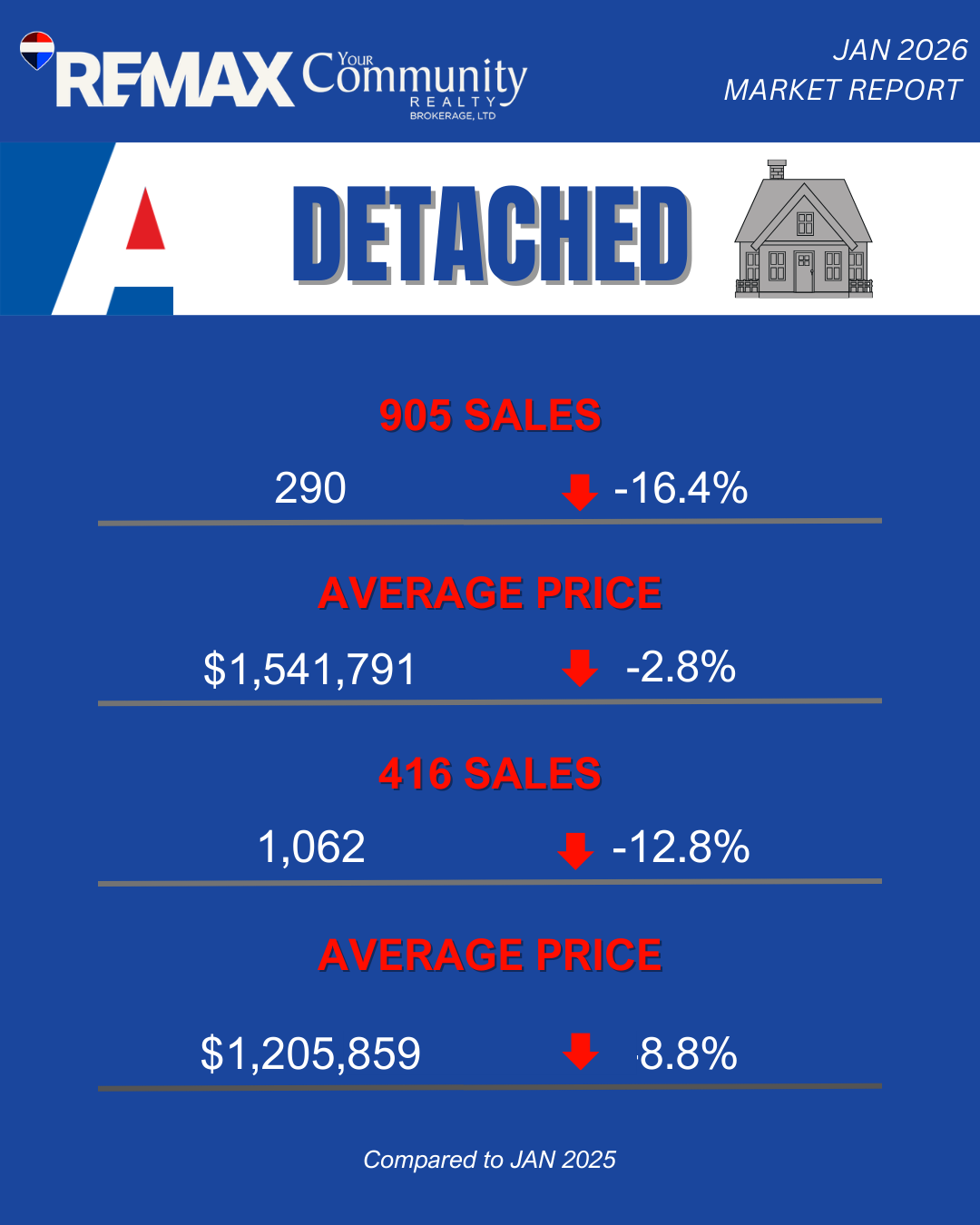

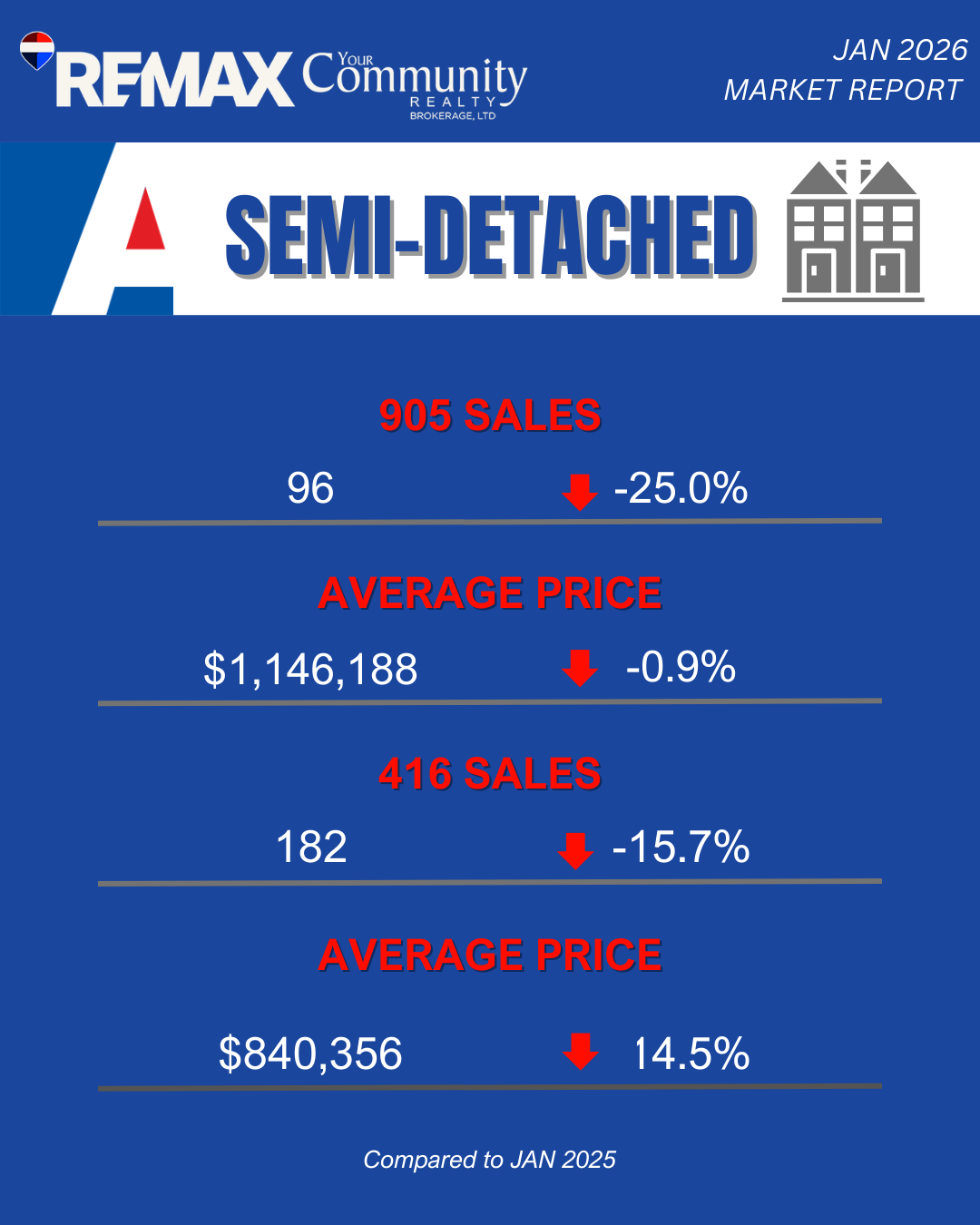

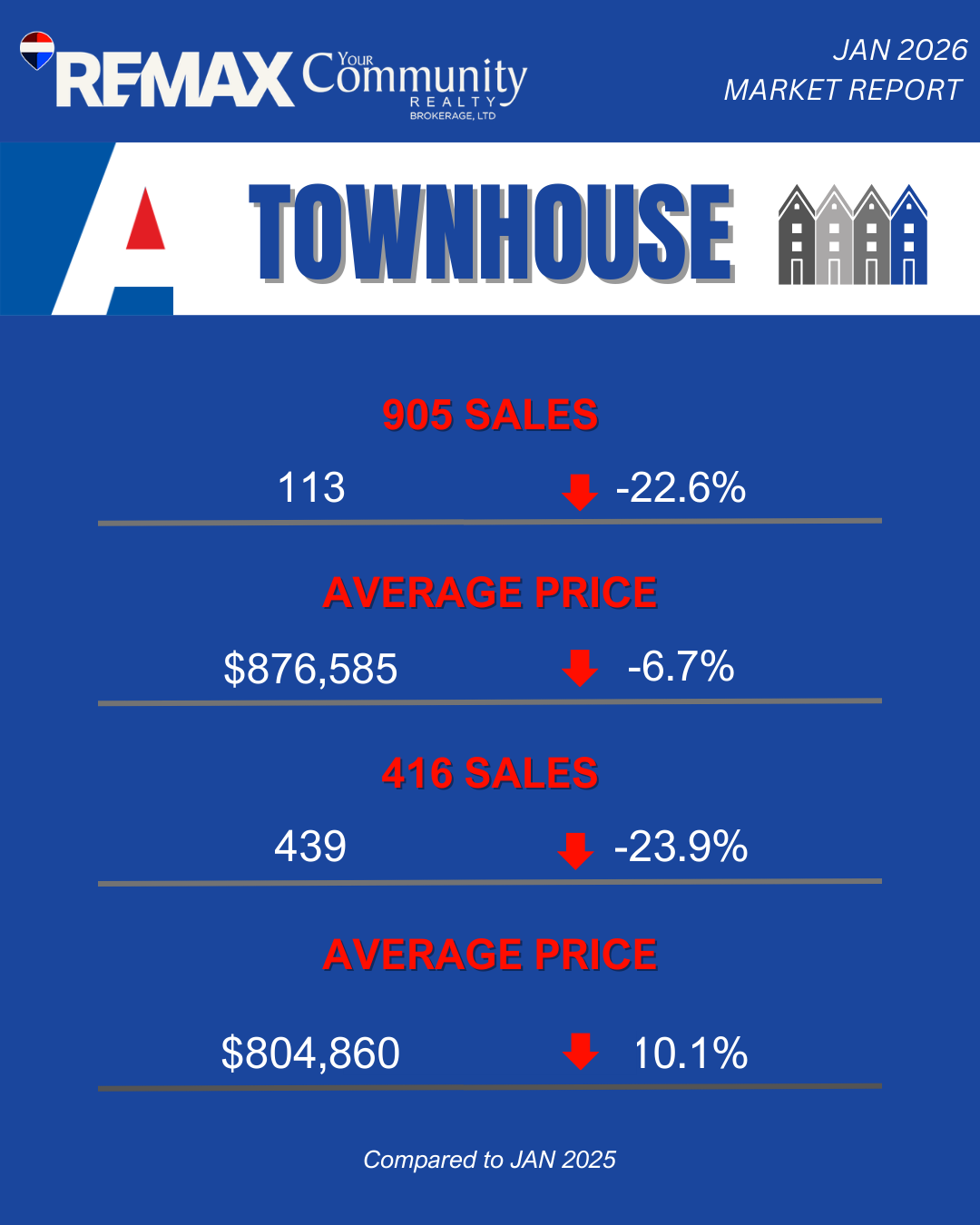

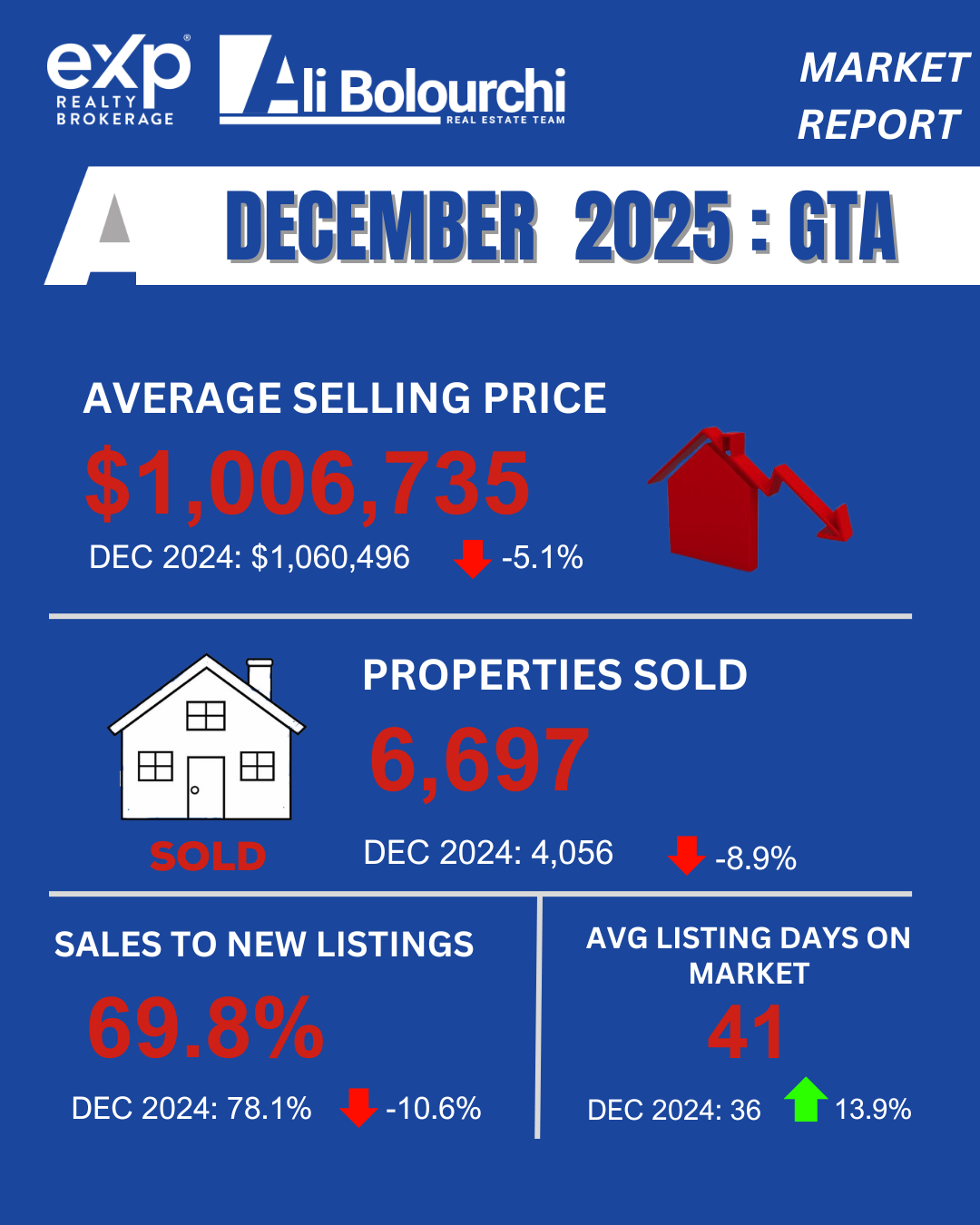

The early months of 2026 have revealed a significant divergence between the performance of core Toronto low-rise housing and the broader suburban and high-rise condominium markets. Data from the first quarter of 2026 indicates that while overall home prices remain approximately 7% below 2025 levels, inventory levels have tightened by 11% year-over-year. This tightening of supply, combined with a relative stabilization of interest rates by the Bank of Canada, has established a floor for property values in high-demand segments, particularly those that support intensification.

| Market Metric | February 2025 | February 2026 | Year-over-Year Change |

| Average Sale Price | $1,084,547 | $1,008,968 | -7.0% |

| Total Transactions | 4,037 | 3,868 | -4.0% |

| New Listings | 12,066 | 10,705 | -11.0% |

| Sales-to-New-Listings Ratio (SNLR) | 33% | 36% | +3.0% |

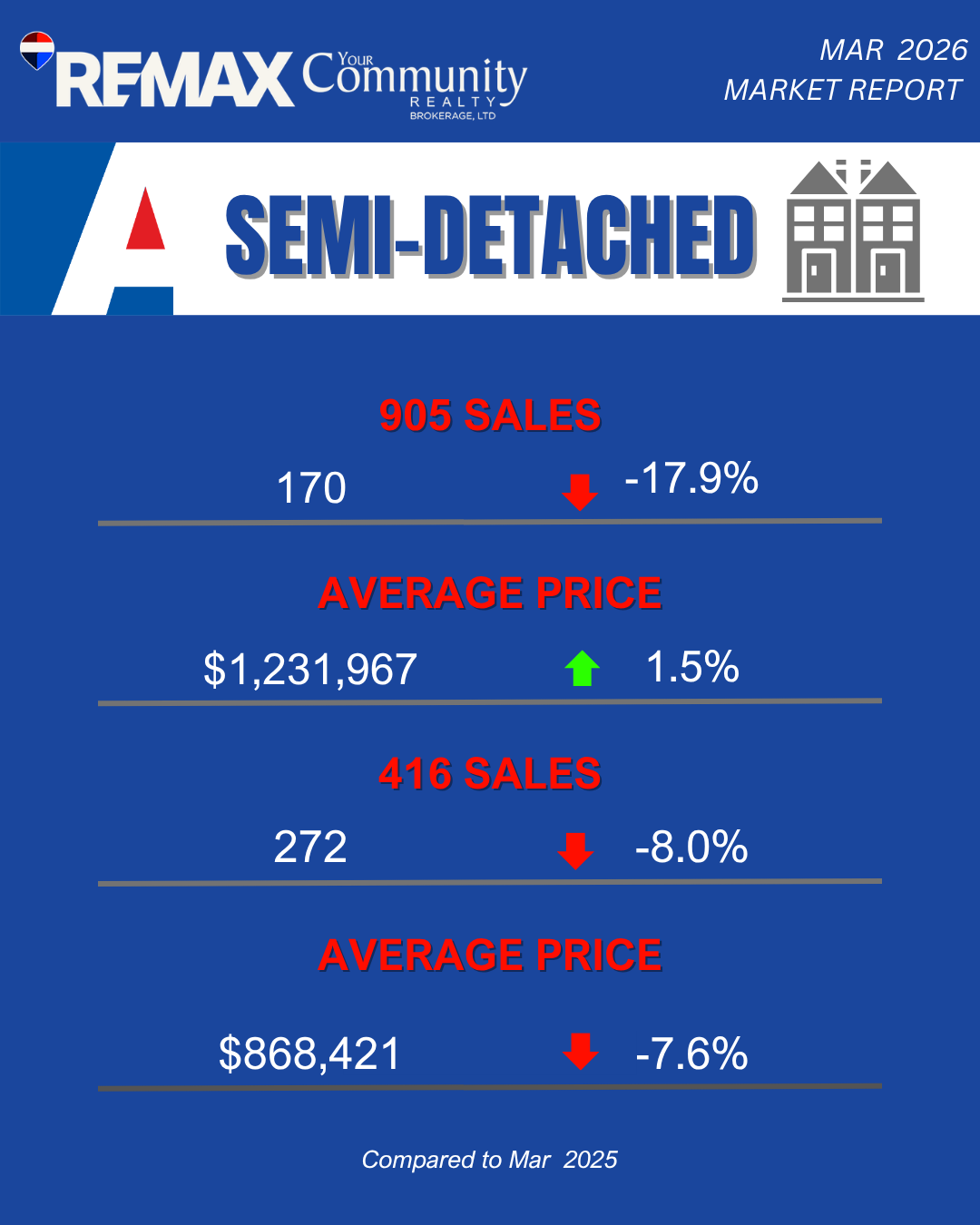

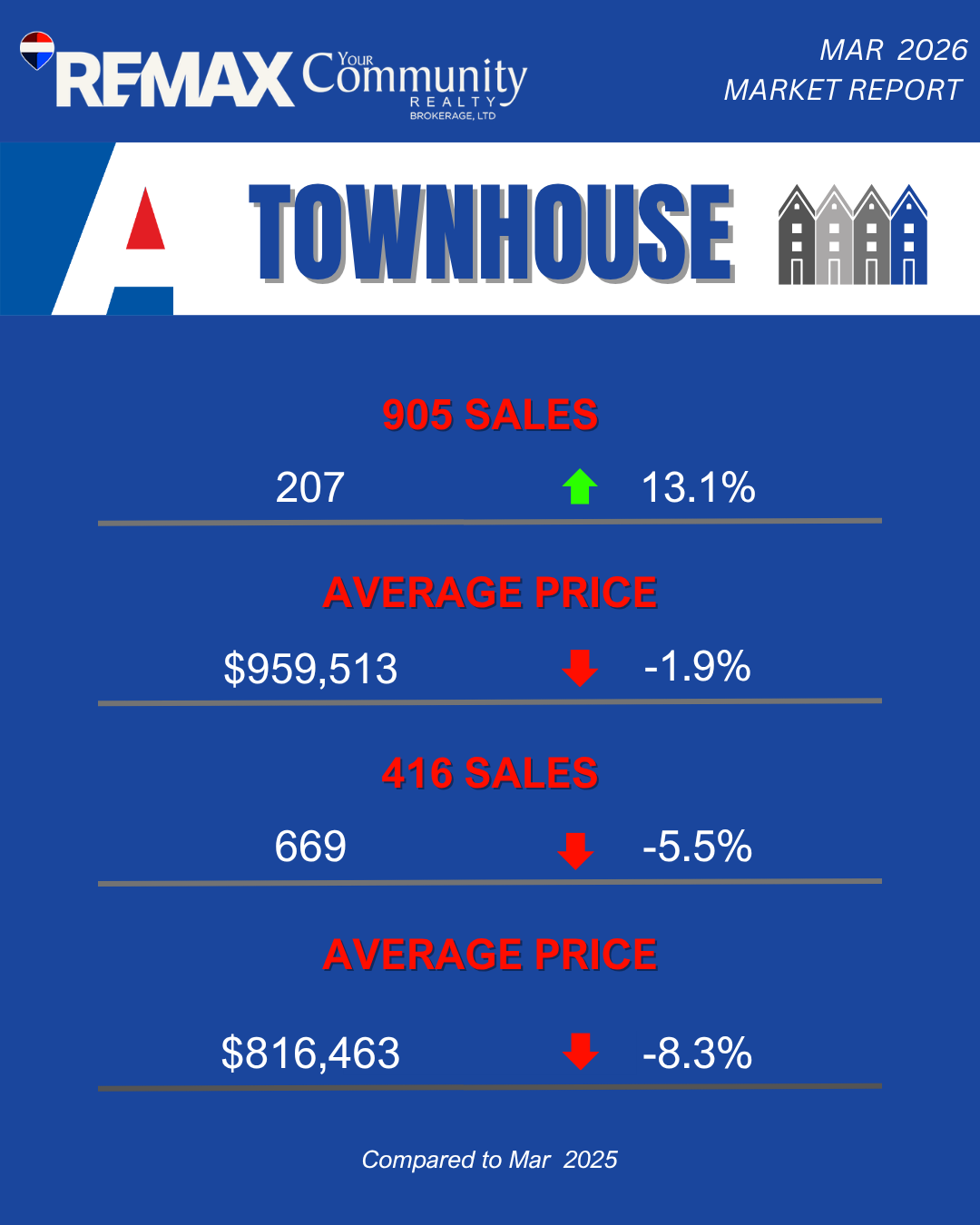

This statistical profile suggests that the market is transitioning from a period of high volatility into a phase of cyclical normalization. The resilience of the semi-detached and detached segments in the 416 area code is particularly noteworthy for strategic investors. These assets serve as the primary inventory for duplex, triplex, and fourplex conversions, maintaining stable demand even as the condominium sector faces a supply overhang and a multi-decade low in pre-construction sales.

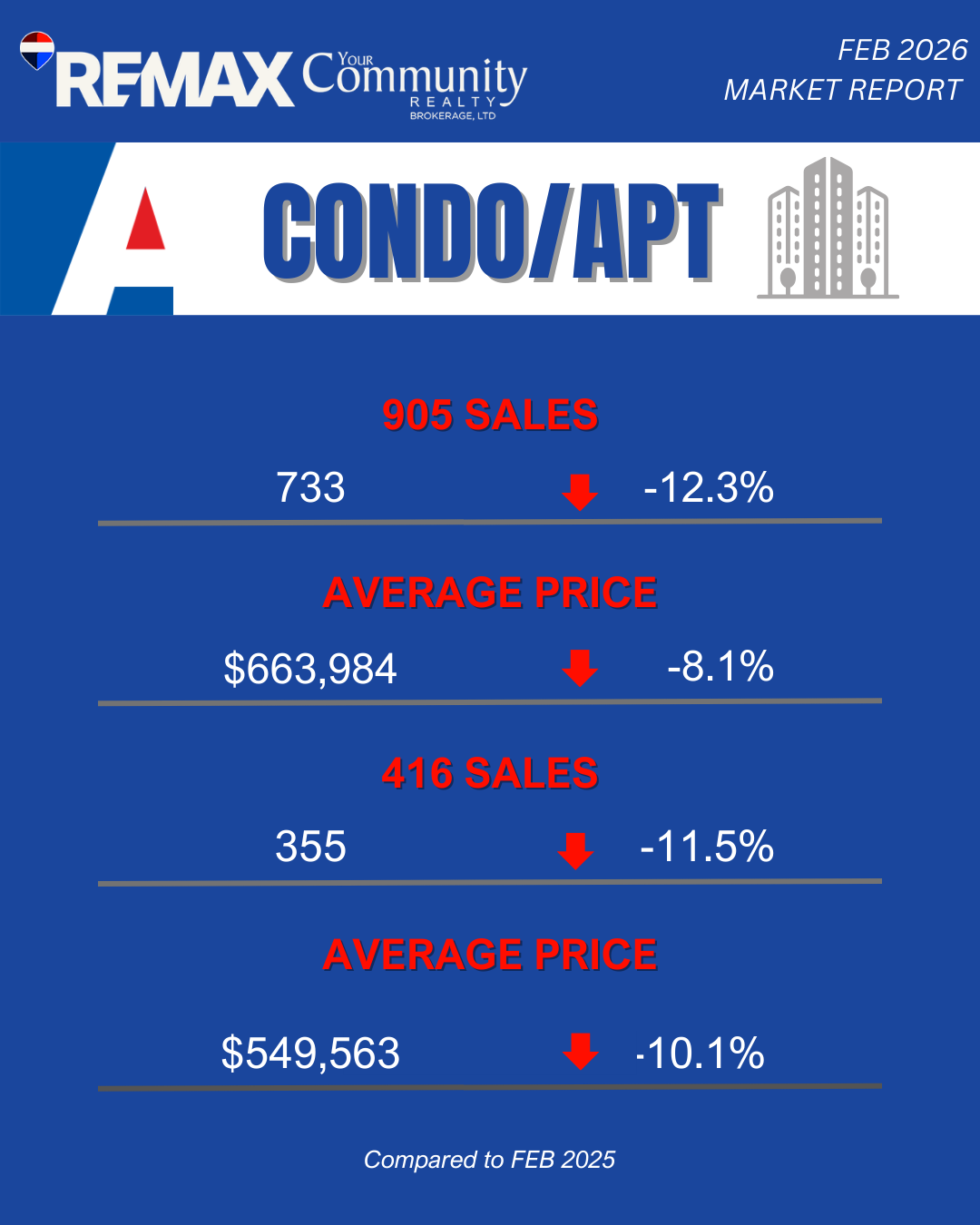

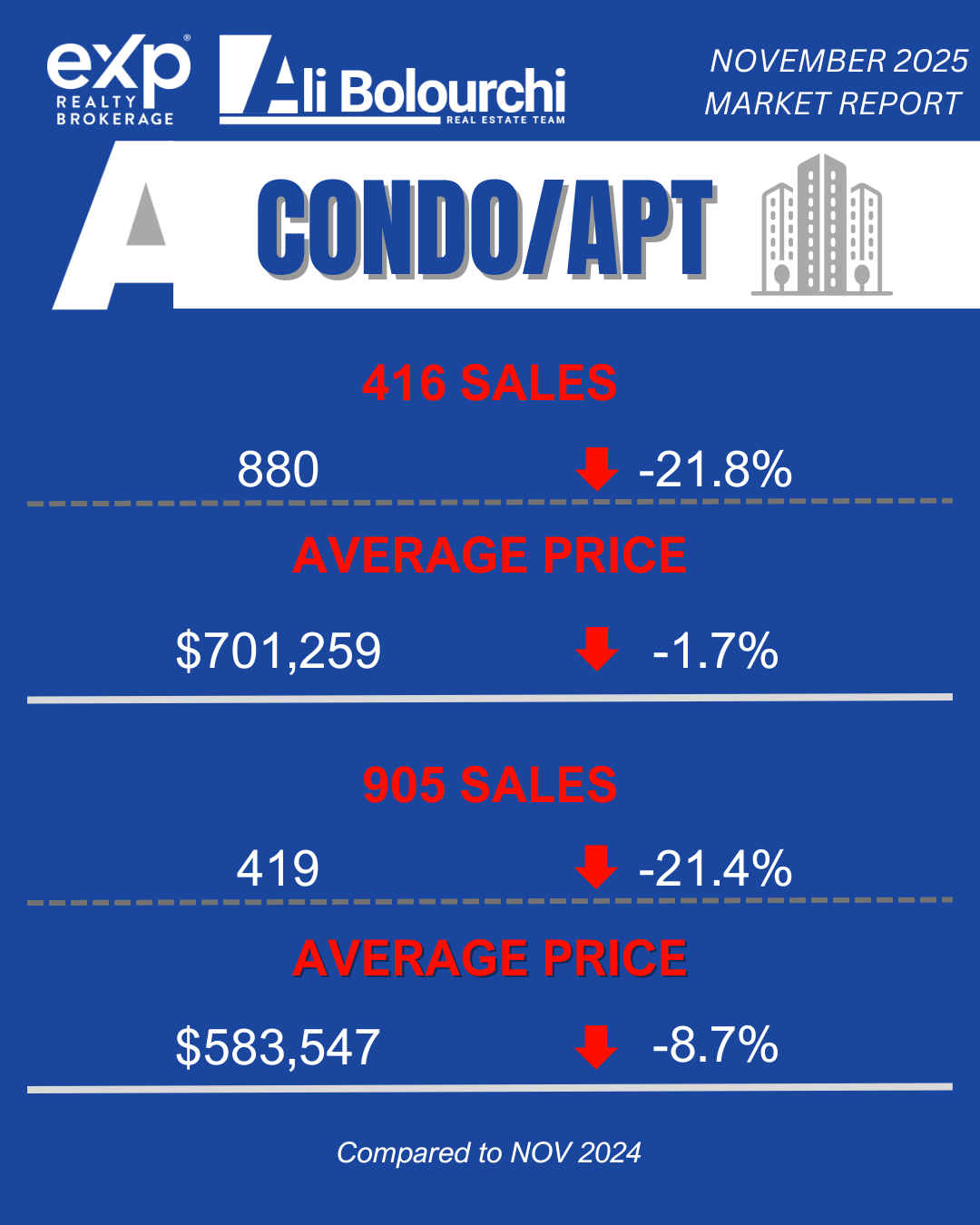

The Realignment of the Condominium Sector

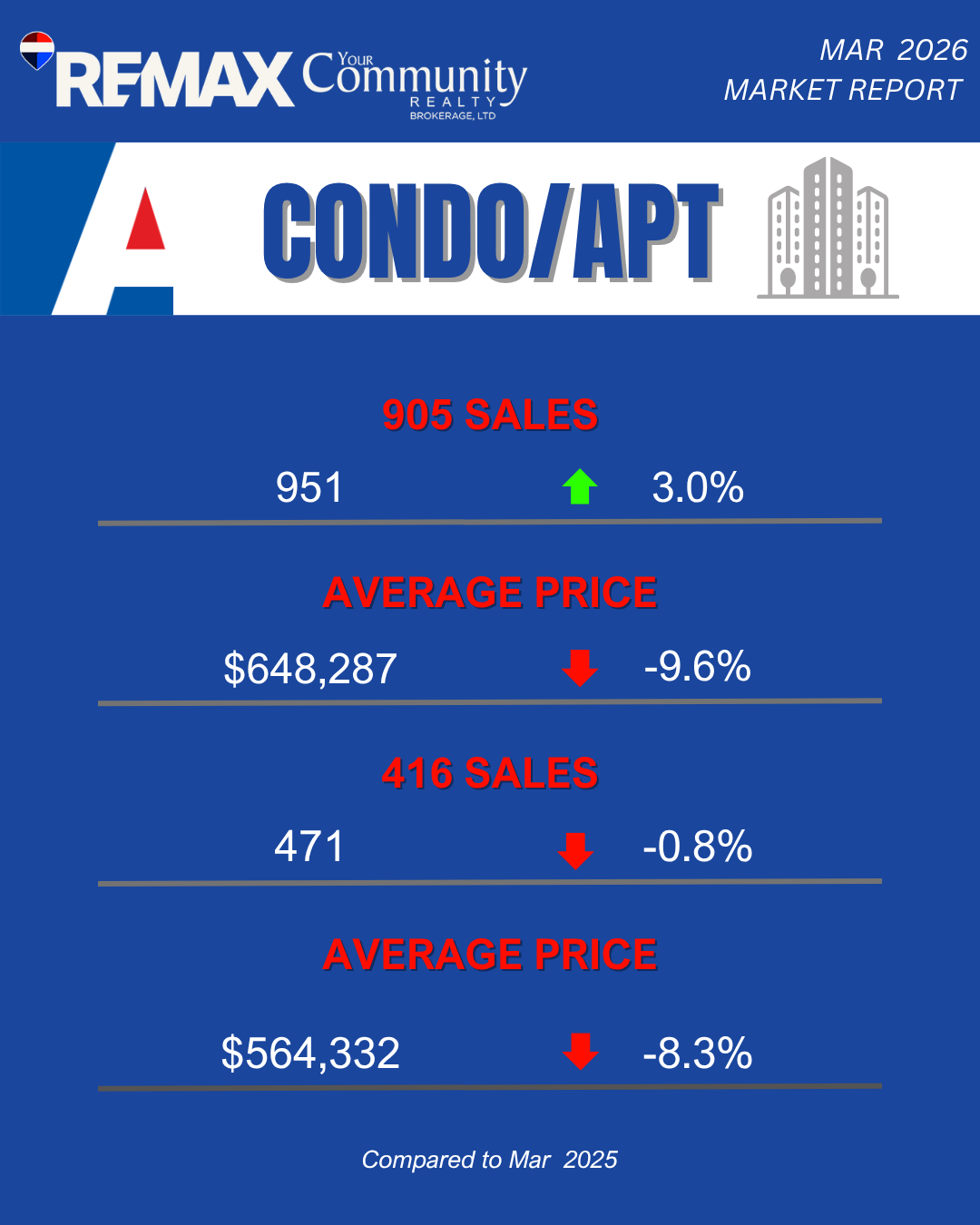

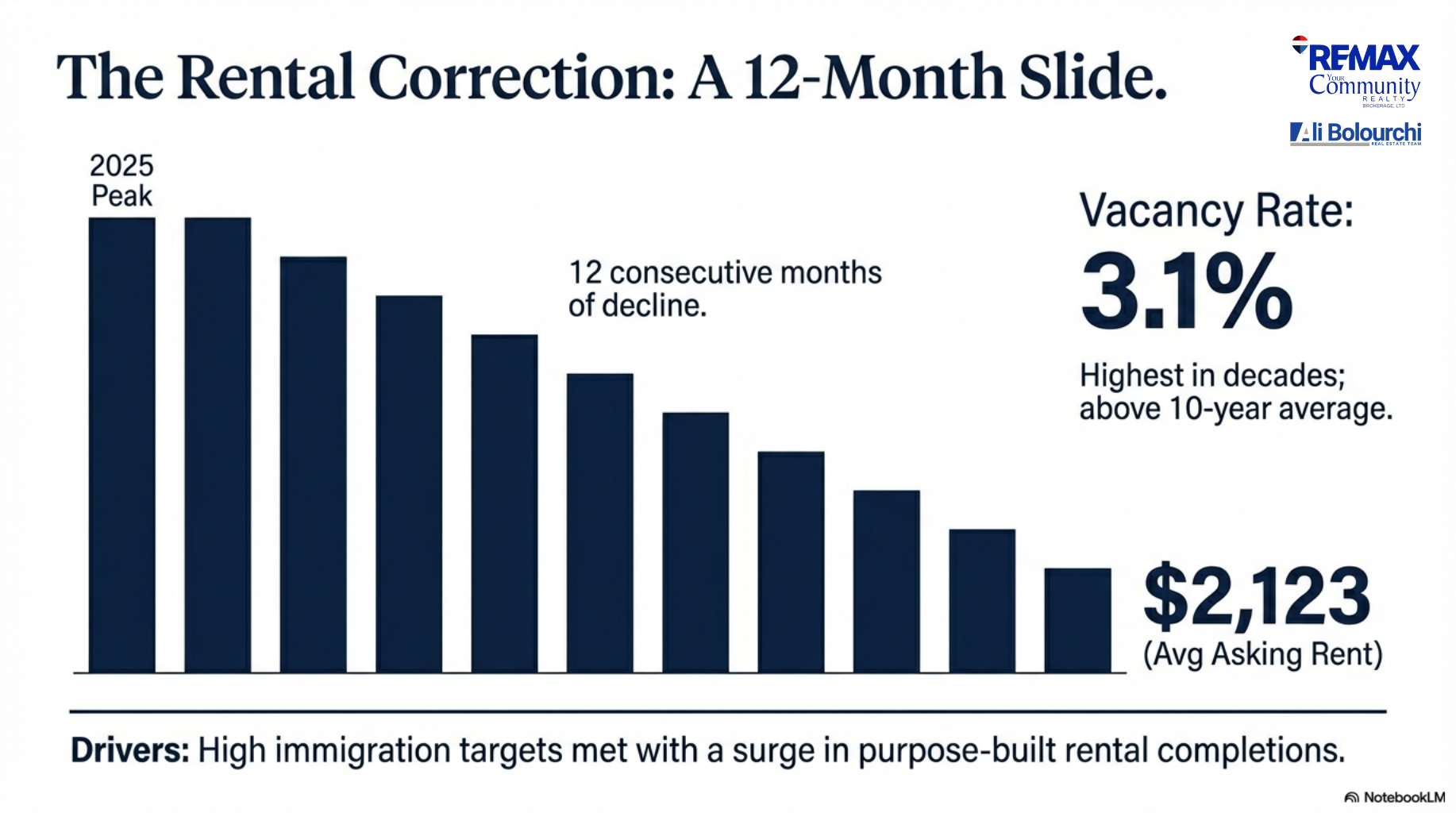

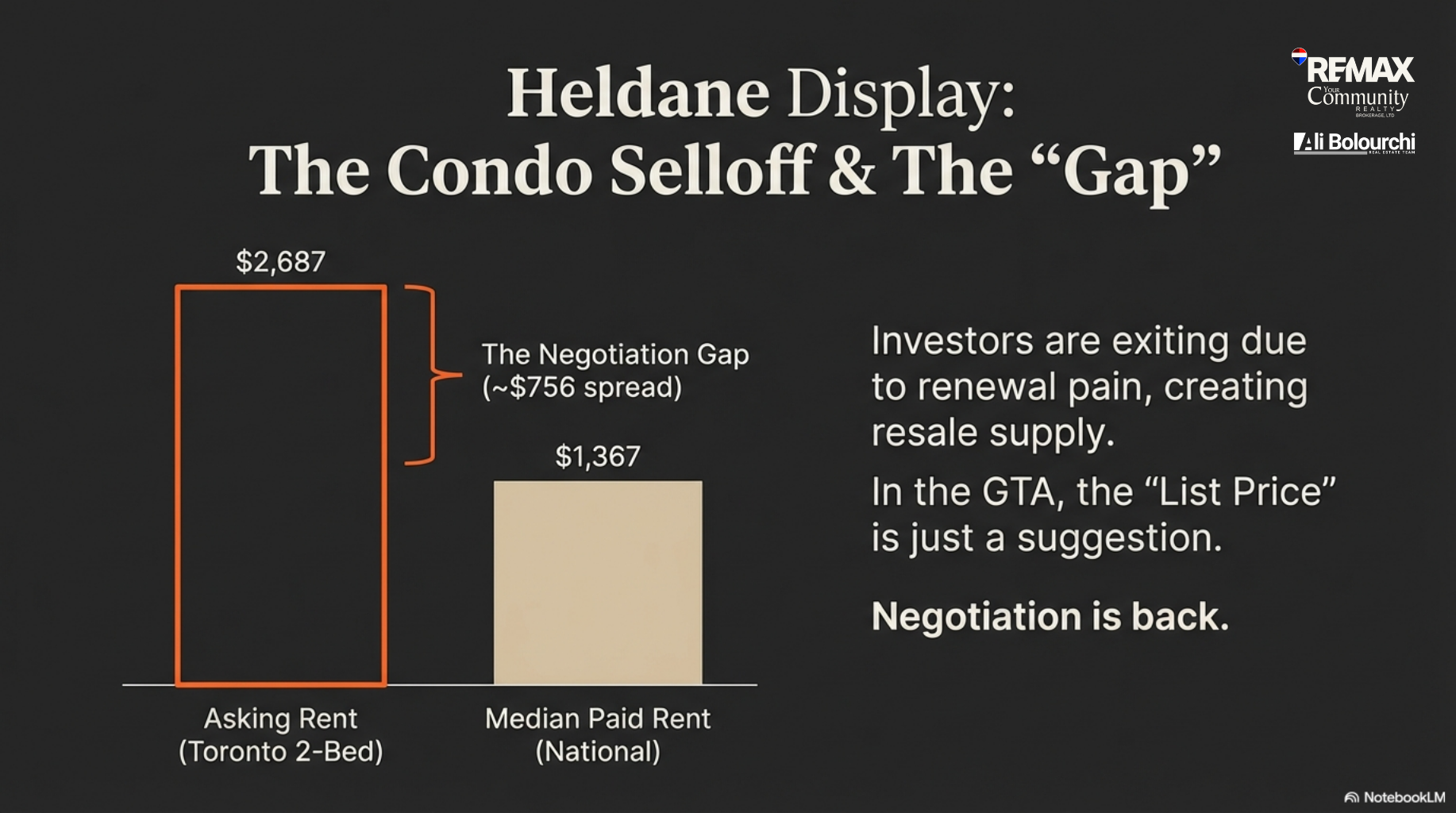

The condominium market in the GTA is currently navigating a period of significant readjustment. High inventory levels, coupled with a surge in secondary rental supply from financially stressed owners, have exerted downward pressure on both sale prices and rental rates. In January 2026, the average price for a condominium in the GTA fell 9.8% year-over-year to $604,759. This softening has led many investors to redirect capital away from single-unit condo investments toward multi-family properties where they exercise greater control over the land and the underlying asset.

The collapse of condominium presales in 2025 has created a vacuum in the future housing pipeline, which is expected to exacerbate supply shortages in the long term. Developers have responded by cancelling high-rise projects or converting them into purpose-built rentals, further emphasizing the shift toward income-producing assets over speculative capital gains.

Missing Middle Construction and Regional Performance Divergence

While high-rise starts have faltered, the construction of missing middle housing—defined as small to mid-scale projects between 4 and 20 units—has shown relative strength. In 2025, missing middle starts rose by approximately 10% across major Canadian metropolitan areas. Toronto has emerged as a leader in this category through conversions, which accounted for more than 21% of all missing middle activity in the city during that period.

| Metropolitan Area (CMA) | Other Missing Middle Starts (%) | Conversions as a Percentage of Total Starts |

| Vancouver | 17.9 | 2.0 |

| Calgary | 43.5 | 12.3 |

| Edmonton | 49.7 | 6.2 |

| Montréal | 26.8 | 5.3 |

| Ottawa | 35.7 | 9.4 |

| Toronto | 15.5 | 21.2 |

| Halifax | 14.9 | 5.8 |

The high rate of conversions in Toronto reflects the maturity of its urban fabric and the regulatory push to add density within established neighborhoods. These projects are often delivered faster than high-rise towers and appeal to a demographic that prioritizes living in established communities with high walk scores and proximity to local businesses.

Regulatory Evolution: The Six-Plex Framework and As-of-Right Development

The most significant regulatory catalyst for GTA investors in 2026 is the expansion of as-of-right zoning for multiplexes. Toronto has transitioned from a period of exclusionary zoning, which historically prioritized single-family detached homes, to a more permissive framework that allows for up to six units on most residential lots in designated wards.

Zoning and Density Allowances

As of early 2026, Toronto allows for the conversion of existing detached or semi-detached homes into multiplexes of up to four units as-of-right across the city, with permissions for up to six units in nine pilot wards. These pilot areas include the former City of Toronto, East York, and parts of Scarborough North. The regulations permit buildings up to four storeys high with a maximum height of 10.5 meters, facilitating taller basement ceilings and improved natural light for lower-level units.

The framework also permits the addition of accessory dwelling units (ADUs), such as laneway or garden suites. In many cases, an investor can achieve seven units on a single lot by combining a six-unit main building with one garden suite. To qualify as a multiplex, at least one unit must be located entirely or partially above another unit; otherwise, the structure is classified as semi-detached or townhouse housing.

Financial Incentives for Residential Densification

To stimulate the development of these units, the City of Toronto has implemented a waiver of development charges (DCs) for the first six residential units on a property. This represents a substantial reduction in upfront costs, as development charges in the GTA can exceed $120,000 for low-rise units. Furthermore, the city has waived parking minimums for small multiplexes, removing the requirement to provide on-site vehicle parking and allowing for more efficient use of the lot for housing.

The economic feasibility of these projects is further enhanced by the Ontario government's policy of waiving development charges for additional units in existing buildings, provided they do not exceed 1% of the existing unit count or one unit, whichever is greater. These combined municipal and provincial measures have made the conversion of underutilized low-rise housing one of the most financially attractive strategies in the 2026 market.

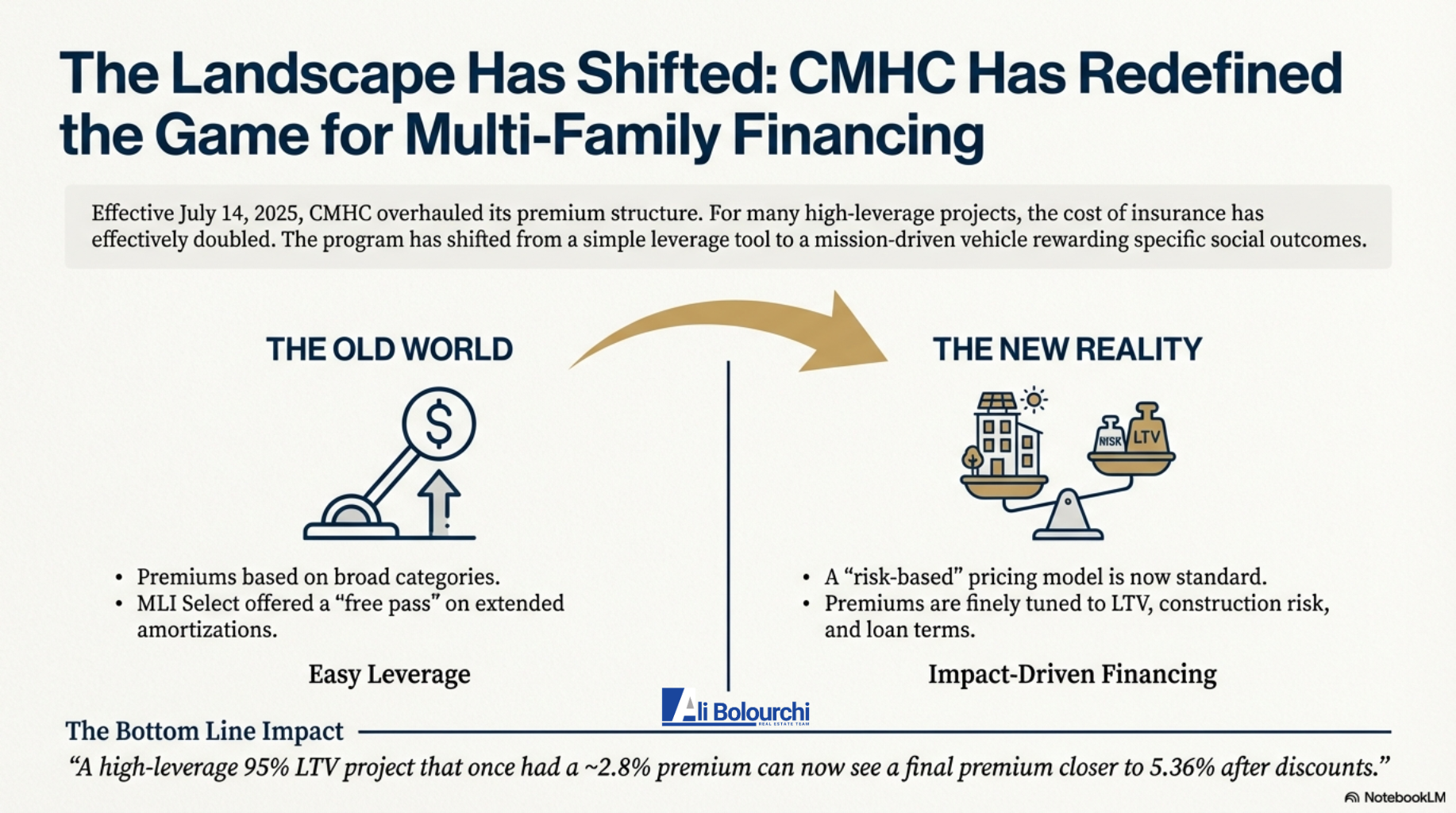

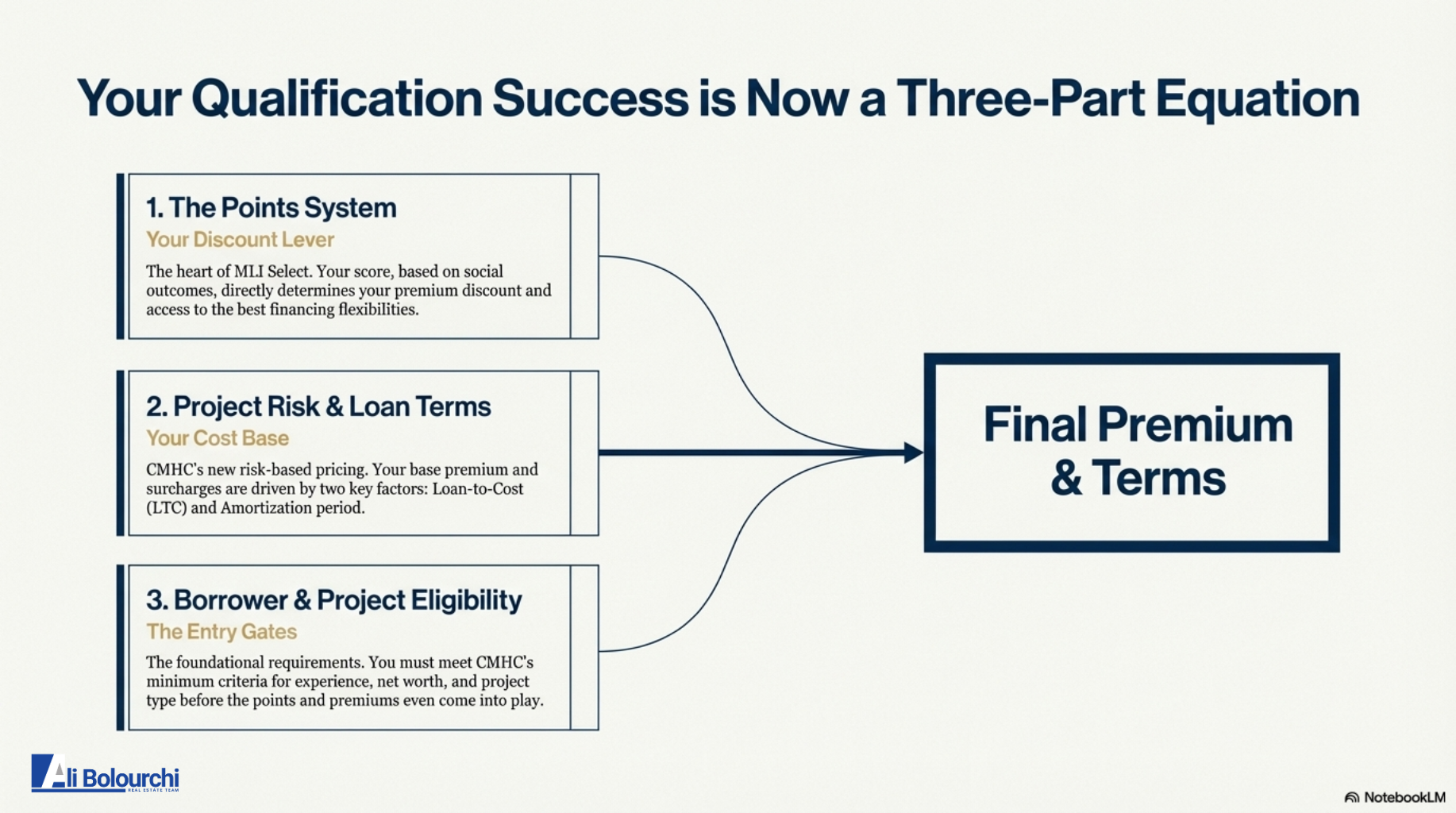

Financial Engineering: Mastery of the CMHC MLI Select Program

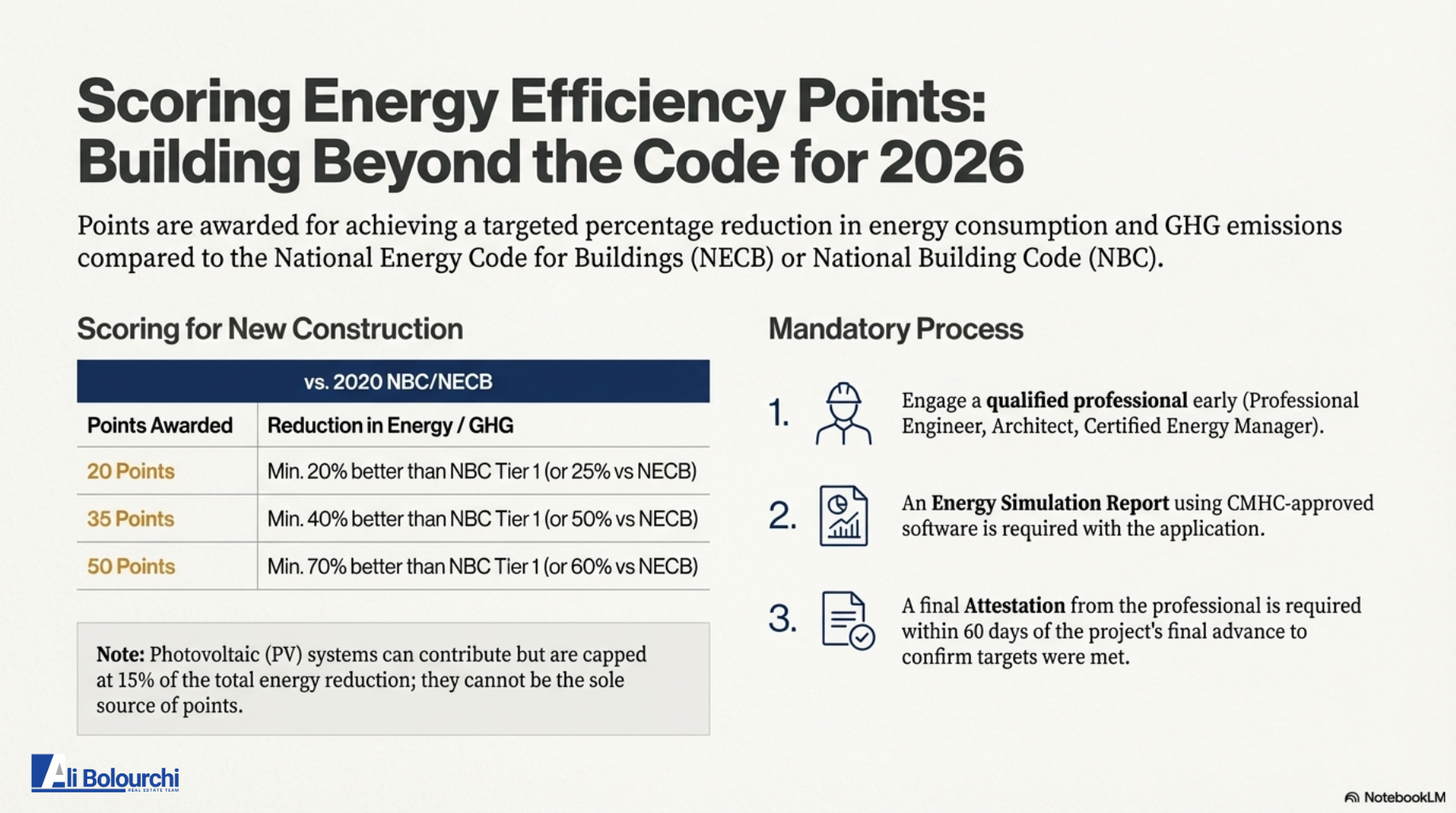

The pivot toward multi-unit investing is inextricably linked to the Canada Mortgage and Housing Corporation (CMHC) MLI Select program. This insurance product has been redesigned in 2025 and 2026 to incentivize the creation of affordable, energy-efficient, and accessible rental housing.

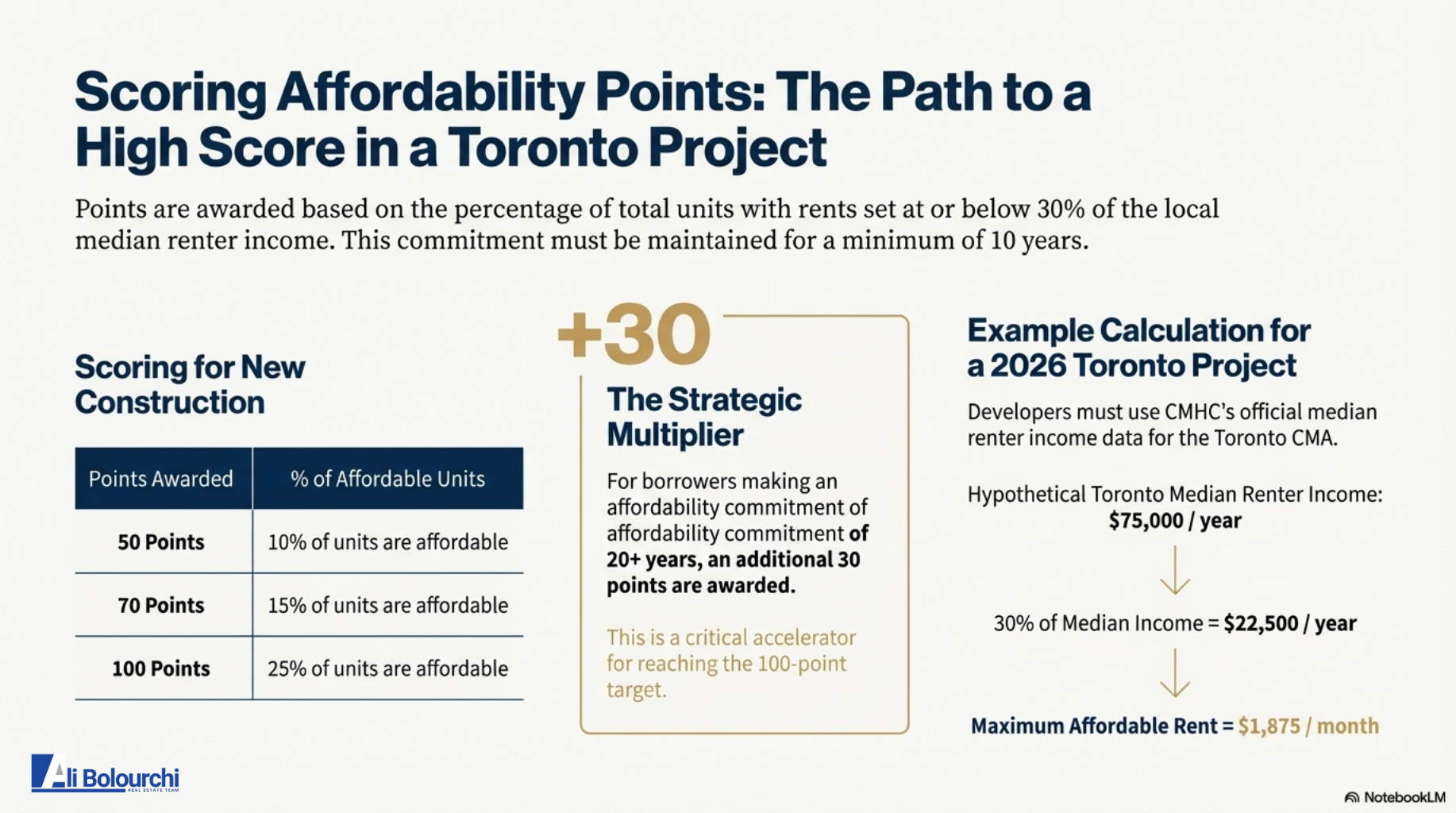

The Points-Based Incentive System

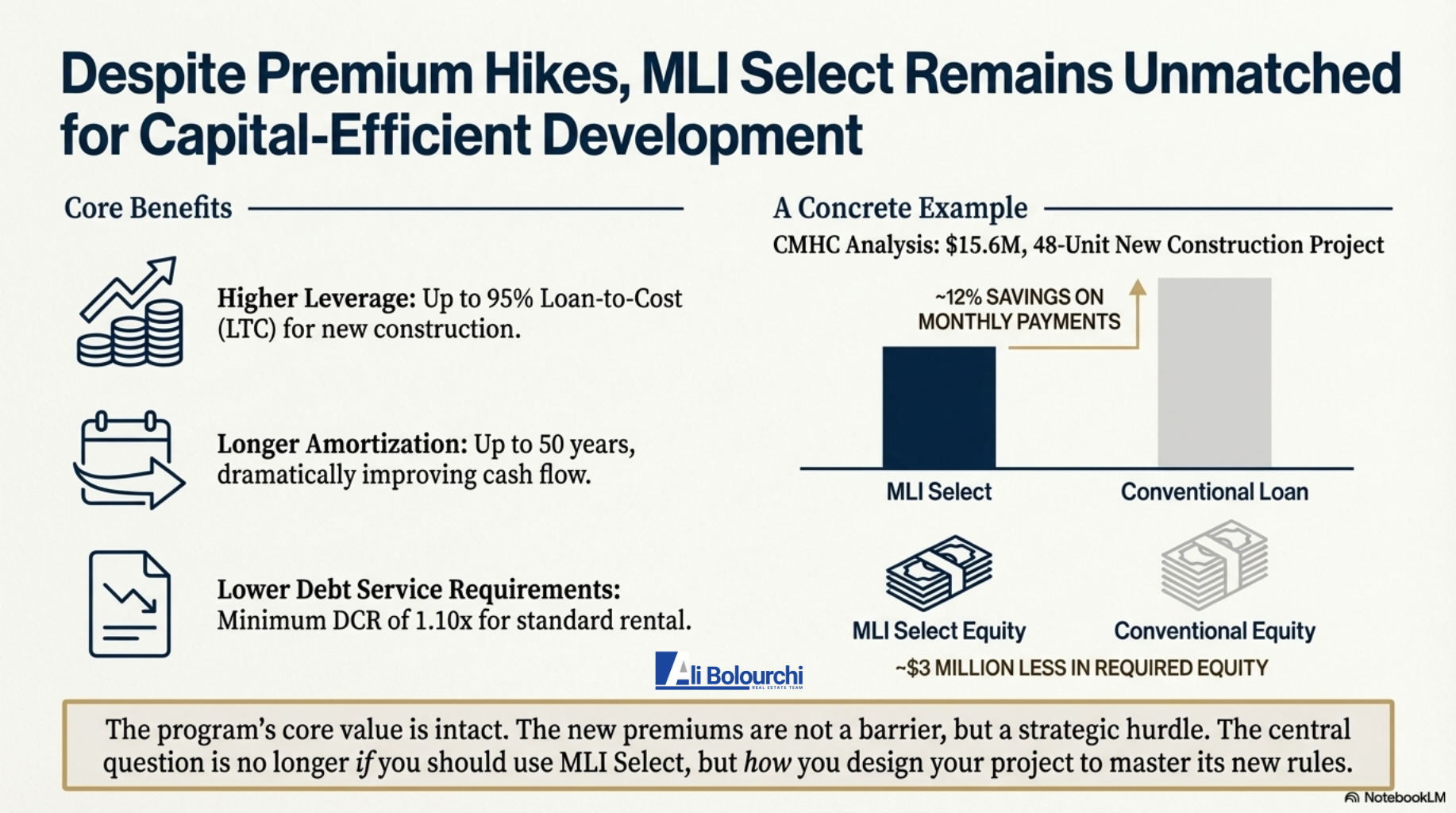

MLI Select utilizes a points-based system to determine eligibility for enhanced financing terms. A project must achieve a minimum of 50 points to qualify, with maximum benefits realized at 100 points or more.

| Financing Feature | 50 Points Tier | 70 Points Tier | 100+ Points Tier |

| Maximum Loan-to-Value (LTV) | Up to 95% | Up to 95% | Up to 95% |

| Maximum Amortization | 40 Years | 45 Years | 50 Years |

| Premium Discount | 10% Discount | 20% Discount | 25-30% Discount |

| Recourse Structure | Full Recourse | Limited Recourse | Limited Recourse |

The scoring criteria are divided into three social outcome categories: affordability, energy efficiency, and accessibility. For example, a project can earn 50 points by committing that 10% of its units will be rented at 30% of the median renter income for the region for a minimum of 10 years. Energy efficiency points are awarded for achieving a 20% to 40% reduction in energy consumption relative to the National Energy Code for Buildings (NECB).

Strategic Implications of 50-Year Amortization and Cash Flow

The ability to access 50-year amortizations through MLI Select is a transformative tool for cash-flow optimization. By extending the repayment period, investors can significantly reduce monthly debt service obligations, thereby increasing the property's net operating income (NOI) and overall return on investment.

For instance, on a $5 million project, the difference between a conventional 30-year amortization and a 50-year insured amortization can amount to thousands of dollars in monthly cash flow savings. This leverage allows investors to scale their portfolios more rapidly by reinvesting the surplus cash flow into additional acquisitions.

Mandatory Surety Bonding and Capital Requirements in 2026

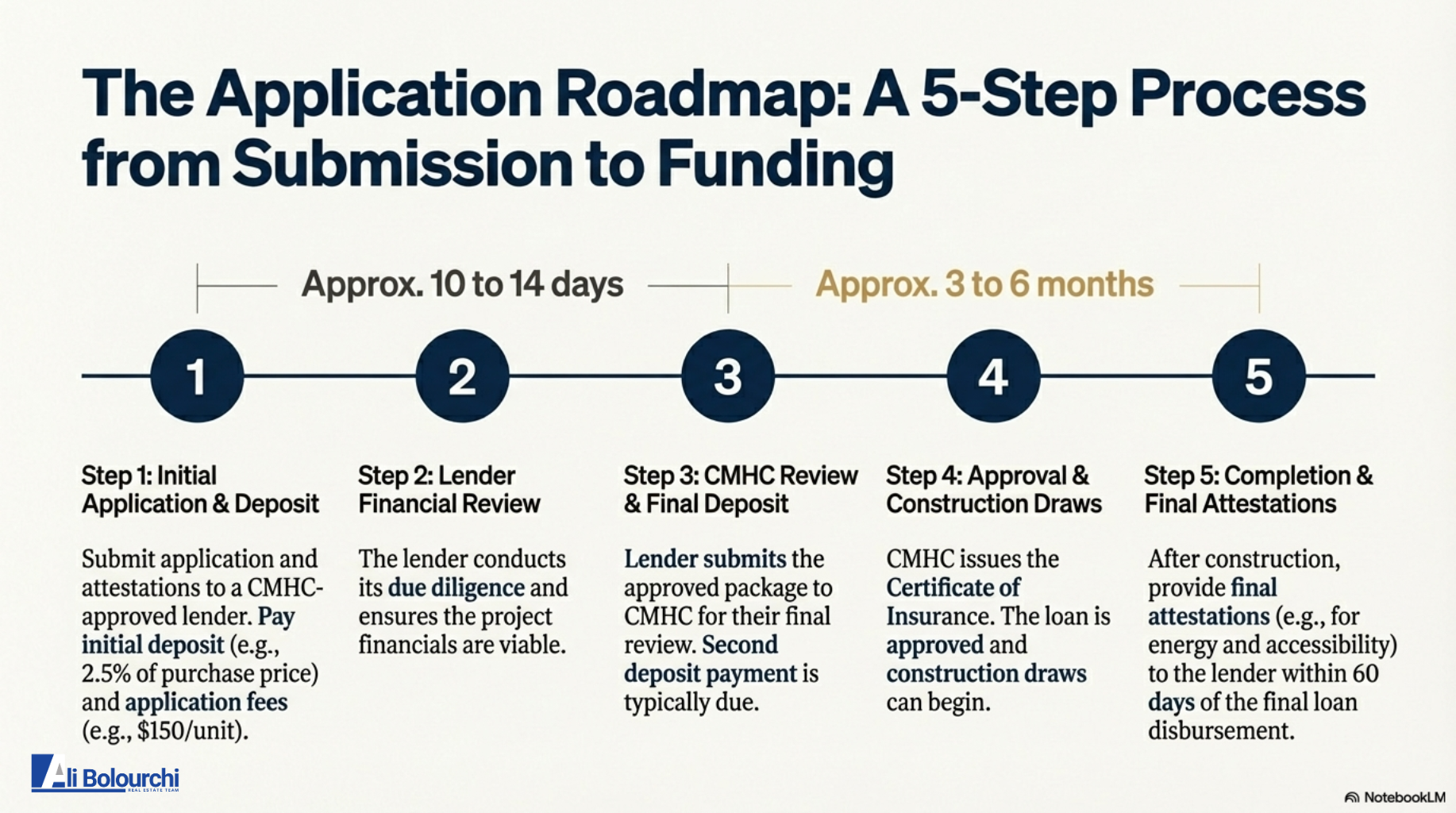

A critical update to the MLI Select program in 2025 and 2026 is the non-negotiable requirement for surety bonding on all construction projects. This applies even to owner-operators and small-scale developers who act as their own general contractors. The bonding must typically include a performance bond covering 50% of the contract value and a labor and material payment bond covering another 50%. These requirements ensure that the project will be completed and that subcontractors will be paid, reducing the risk for both the lender and CMHC.

Investors must also be prepared for significant upfront capital requirements. While MLI Select offers up to 95% financing, construction draws are typically paid out in stages. In many cases, an investor must cover approximately one-third of the total project costs in cash before the first draw is released. This necessitates a robust balance sheet and often requires the use of bridge or private financing during the initial construction phase.

The Strategic Real Estate Advisor Persona: Precision and Calculated Confidence

In the 2026 market, the role of the real estate professional has evolved from a transactional agent to a high-level strategic advisor. This model, exemplified by the ABRE Team, emphasizes the use of data-driven industrial engineering principles to optimize financial outcomes for clients.

Industrial Engineering and Market Foresight

The integration of industrial engineering methodologies allows for the precise analysis of the "time value of money" and "process optimization" in real estate transactions. This approach is designed to eliminate the guesswork and emotional paralysis that often hinder investors in complex markets like the GTA. By utilizing an 8-Point Segmented Market Analysis, a strategic advisor can provide precision data specific to a client's street or asset class, rather than relying on broad, often contradictory city-wide statistics.

Empathy-Driven Copywriting and Intent-First Communication

Modern real estate advisory also requires a sophisticated approach to communication. This involves shifting away from traditional sales scripts toward "calculated confidence" and "empathy-driven" messaging. The objective is to speak directly to the target audience's needs and fears—such as the fear of financial regret or the vulnerability caused by market opacity.

Content strategy must align with search intent, focusing on narrow, "winnable" topics that attract qualified prospects. A 9-step SEO system can be utilized to ensure that social posts and blog content are scannable, value-rich, and optimized for both humans and search engines.

Identifying Investor Psychology in the 2026 GTA Market

The contemporary investor profile in the GTA has shifted significantly in response to the volatility of the early 2020s. The ideal customer is now identified as the "Ambitious Mainstream Strategist"—financially stable, budget-conscious individuals between the ages of 28 and 55 who view real estate as their primary vehicle for long-term wealth building.

Core Problems and Internal Motivations

The primary external problem facing these investors is market opacity. They are inundated with contradictory statistics and lack the precise, segmented data needed to take decisive action. Internally, they are driven by a profound fear of financial regret—specifically the fear of buying at the peak of a cycle, selling at a low, or acquiring a flawed asset.

Philosophically, these individuals believe that hard-working people deserve a clear, strategic path to build wealth, but they feel the current market is often "rigged for insiders". They are frustrated by the time wasted on ambiguous news that is not specific to their localized street or asset class.

The Demand for Guidance over Sales

Investors in 2026 no longer respond to the pushy, high-pressure salesperson. While some may mistake aggression for effectiveness, the most successful advisors counter this by delivering "Calculated Confidence" through data. The repetitive question in the market is no longer "How high can this go?" but rather "Is now really the right time to act, or should I wait for the next rate cut?".

The ABRE Team approach addresses this by moving from selling to guiding. This involves simplifying complex processes and data, ensuring that every strategic recommendation is backed by objective economic analysis rather than personal commission-driven urgency.

The Project Lifecycle of a Toronto Multiplex Conversion

To successfully execute the strategies discussed in these blogs, investors must understand the operational realities of the 2026 conversion market. The process is governed by a combination of the Ontario Building Code, municipal by-laws, and federal insurance requirements.

Budgeting and Timelines for Multiplex Development

Successful projects require a rigorous approach to project management. Construction costs, while off their pandemic peaks, remain elevated, requiring precise budgeting for materials and labor.

| Project Stage | Estimated Timeframe | Cost/Requirement |

| Zoning Review Application | 1 Month+ | $600 - $2,000 |

| Design & Detailed Drawings | 2 - 4 Months | $10,000 - $30,000 |

| Committee of Adjustments | 3 - 6 Months | $5,000+ (If Required) |

| Building Permits and Fees | 1 - 2 Months | $10,000 - $20,000+ |

| Multiplex Conversion Work | 3 - 12 Months | $40,000+ per unit |

| New Multiplex Build | 12 - 24 Months | $250 - $400 / sq. ft. |

| Surety Bonding | Pre-Construction | 10% of Hard Costs |

Technical Compliance: Part 9 of the Building Code

One of the natural advantages of missing middle projects is their ability to utilize "Part 9" construction standards. This streamlined section of the Building Code applies to housing and small buildings, allowing developers to undercut the complex and expensive cost structures required for high-rise towers. To qualify as a multiplex under these rules, each unit must have a private entrance, a kitchen, and a bathroom.

Effective February 16, 2026, all building permit applications in Toronto must utilize an updated "Application for a Permit to Construct or Demolish" form. Drawings must be submitted on standardized sheets, fully dimensioned, and often require the seal of a professional engineer. For renovations of residential units, a "Rental Renovations License" may also be required under Toronto Municipal Code Chapter 662 to protect tenant rights during the conversion process.

Performance Metrics: The Cap Rate Formula

In the multiplex sector, property value is driven primarily by income potential rather than simple comparable sales. Investors utilize the capitalization rate (cap rate) to assess the feasibility of a deal.

In the 2026 Toronto market, smaller multiplex properties typically trade at cap rates between 5.0% and 5.5%. For a turnkey triplex generating $6,000 per month in rent, the resulting income returns are often comparable to much larger, more complex projects but with significantly lower execution risk.

Conclusion: Synthesis of the 2026 Investment Outlook

The research indicates that the Greater Toronto Area real estate market in 2026 is defined by a shift toward resilient, income-producing assets. The return of the missing middle is not merely a trend but a structural response to the failure of the high-rise condominium model to meet the needs of families and long-term investors.

The successful investor in this era is one who moves from guesswork to "Calculated Confidence" by leveraging industrial engineering principles and precision market data. By mastering the CMHC MLI Select program—including its complex points system and mandatory bonding requirements—investors can access unprecedented leverage, such as 95% LTV and 50-year amortizations, to scale their portfolios.

The suggested blog titles provide a roadmap for communicating these high-level strategic insights to a market that is increasingly skeptical of traditional sales tactics. By focusing on intent-first, data-driven content, real estate professionals can position themselves as the necessary guides for the "Ambitious Mainstream Strategist," transforming underutilized residential lots into multi-generational "equity machines".