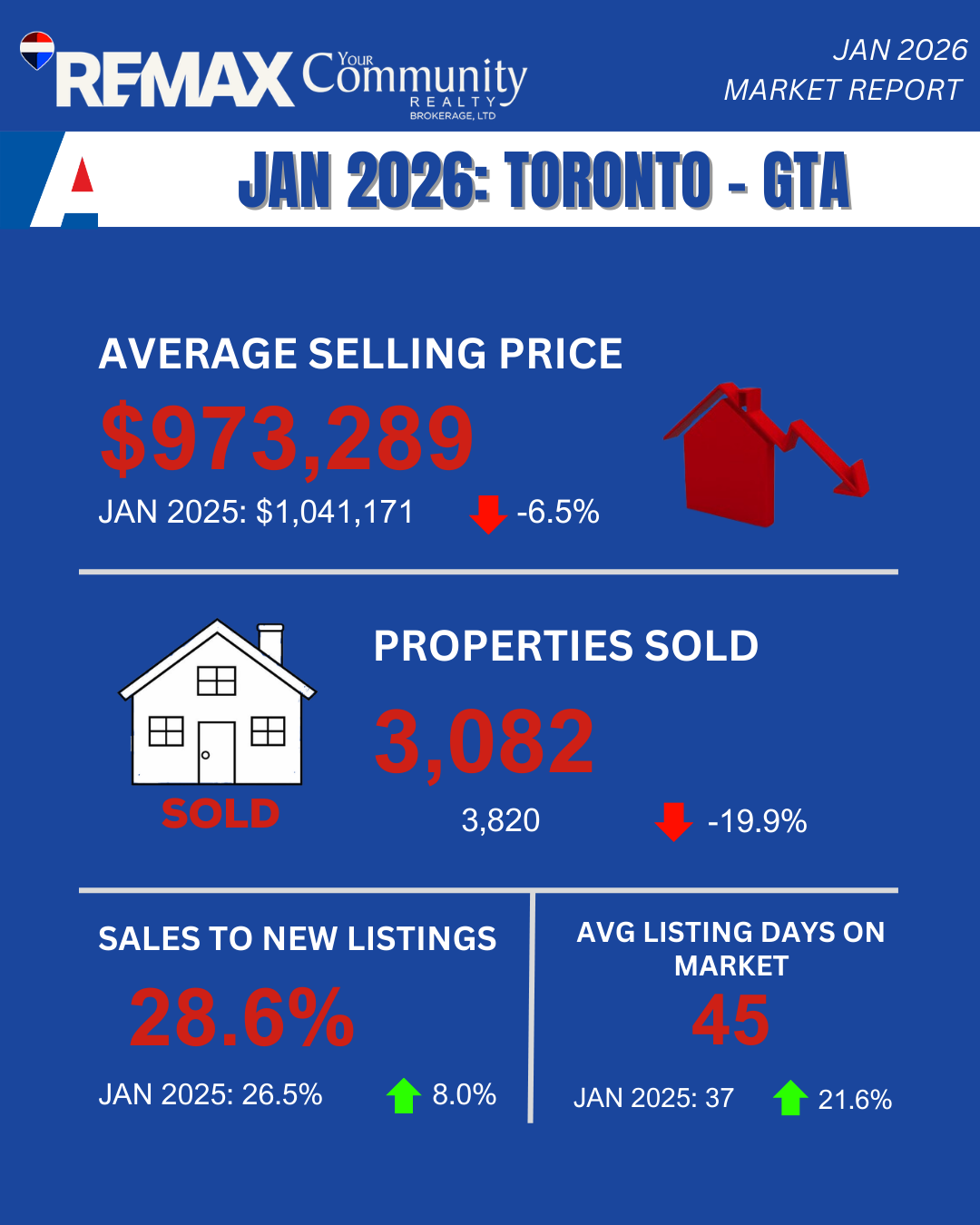

Welcome to 2026! The Greater Toronto Area (GTA) housing market kicked off the new year with a noticeable chill, bringing both challenges for sellers and incredible opportunities for buyers.

According to the latest TRREB data, there were 3,082 home sales reported in January—a significant 19.3% drop compared to January 2025. But the real headline? The average selling price across the GTA has dipped below the $1 million mark, landing at $973,289 (down 6.5% year-over-year).

While new listings entering the market also decreased by 13.3% , month-over-month trends show prices and the MLS® HPI composite are continuing to trend lower. We are firmly in a market where pricing strategy is everything.

Here is a deep dive into how the 416 (City of Toronto) and 905 (Suburban GTA) markets performed by property type in January 2026.

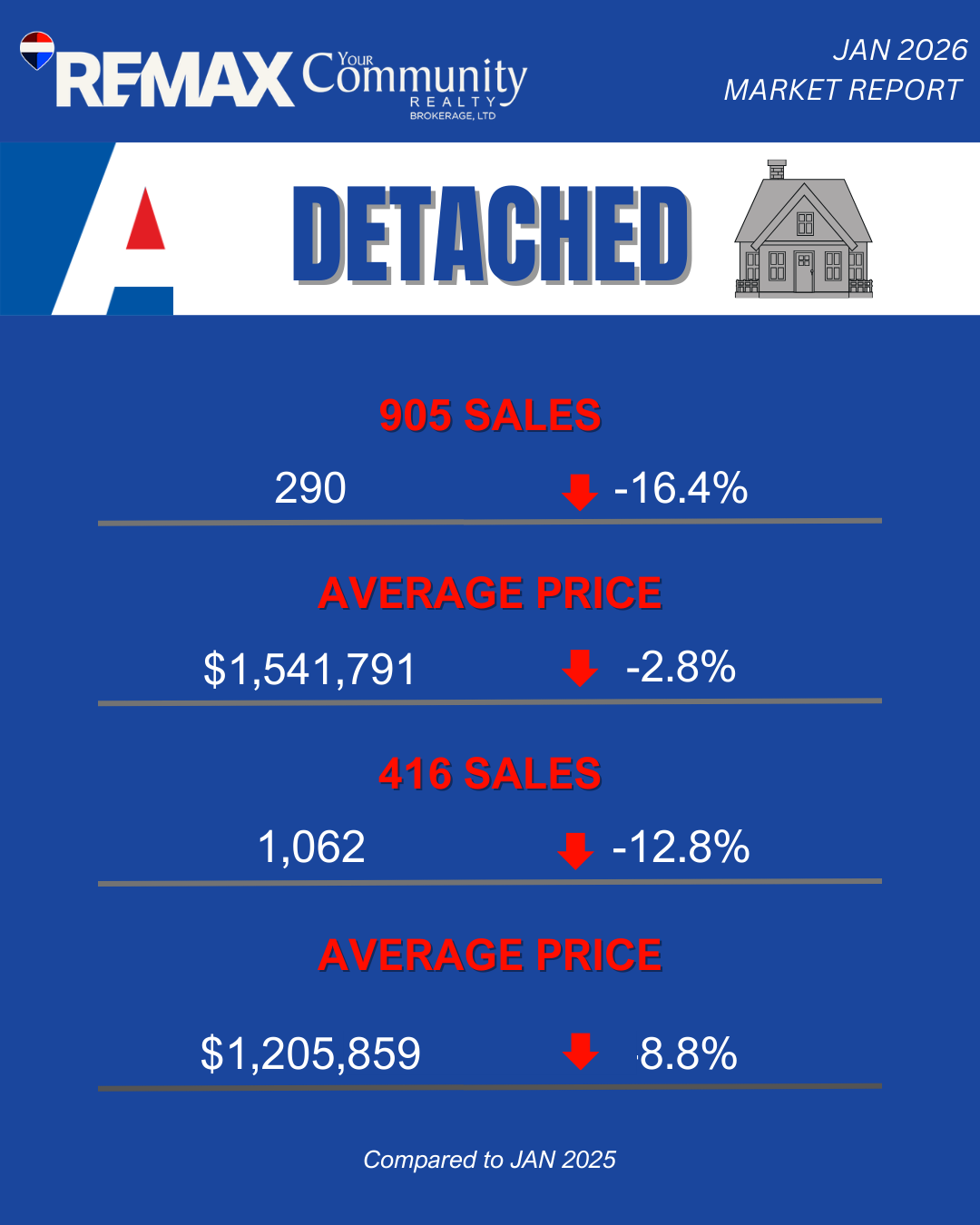

🏡 Detached Homes

The detached market remains the gold standard for GTA living, but buyers are finding much more breathing room, especially outside the city core.

416 (Toronto Core)

Average Price: $1,541,791.

Trend: Down 2.8% year-over-year. The city's detached market is holding its value better than the suburbs, though prices are still softening.

905 (GTA Suburbs)

Average Price: $1,205,859.

Trend: Down 8.8% year-over-year.

Insight: The suburban premium has officially cooled. For families looking to upsize, the 905 region is offering substantial discounts compared to last year, making this a prime window to negotiate a forever home.

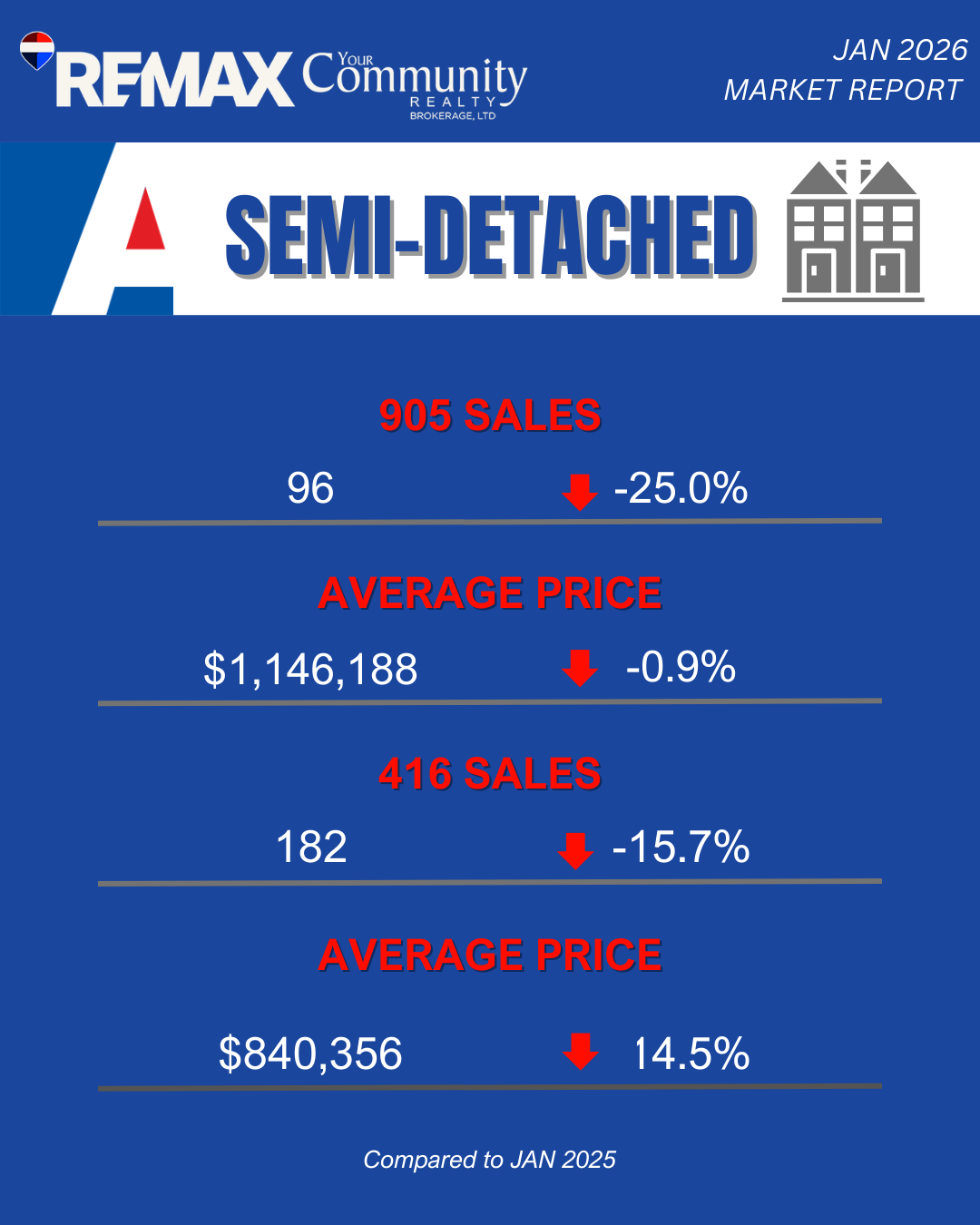

🏘️ Semi-Detached Homes

Semi-detached homes saw some of the most dramatic differences between the city and the suburbs this month.

416 (Toronto Core)

Average Price: $1,146,188.

Trend: Down just 0.9% year-over-year. City semis remain incredibly resilient and highly sought-after.

905 (GTA Suburbs)

Average Price: $840,356.

Trend: Down a massive 14.5% year-over-year.

Insight: If you are a first-time buyer or investor, suburban semis are flashing a massive "buy" signal. With average prices dropping to the mid-$800s in the 905, this segment represents some of the best value in the current market.

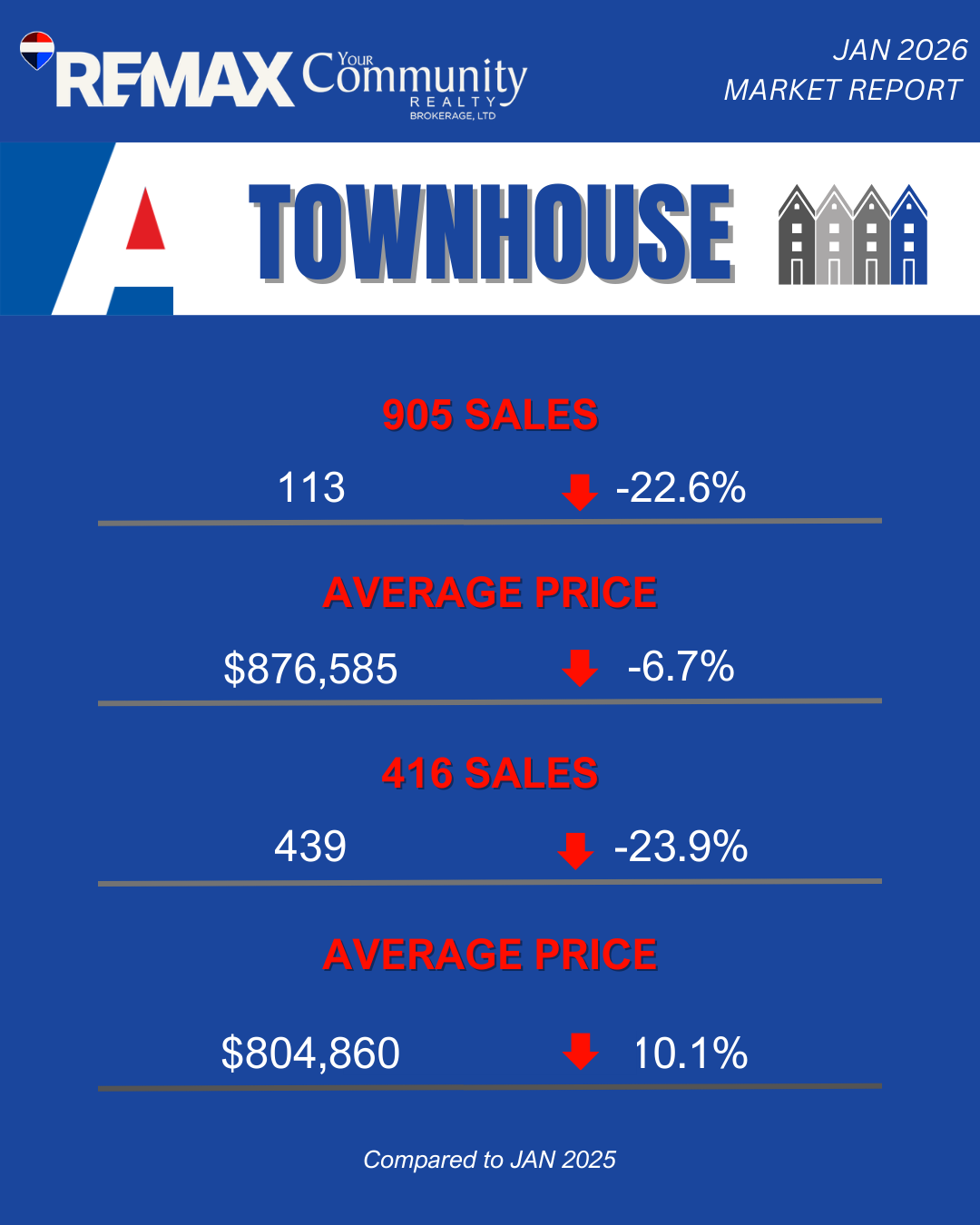

🏙️ Townhouses

Townhomes, often the "missing middle" of housing, saw a fairly even price correction across the board as affordability constraints continue to dictate buyer behavior.

416 (Toronto Core)

Average Price: $876,585.

Trend: Down 6.7% year-over-year.

905 (GTA Suburbs)

Average Price: $804,860.

Trend: Down 10.1% year-over-year.

Insight: The price gap between a city townhouse and a suburban townhouse has narrowed to roughly $70,000. Buyers who were previously pushed to the suburbs might find they can afford to stay in the 416 right now.

🏢 Condo Apartments

The condo sector continues to face headwinds. As inventory sits, sellers are being forced to aggressively adjust their expectations to get deals done.

416 (Toronto Core)

Average Price: $631,932.

Trend: Down 8.6% year-over-year.

905 (GTA Suburbs)

Average Price: $551,166.

Trend: Down 13.0% year-over-year.

Insight: Condo buyers currently have the luxury of choice and time. With 905 condos hovering near the $550k mark, the barrier to entry for homeownership is the lowest it has been in quite a while. Sellers in this space must ensure their units show perfectly and are priced competitively from day one.

Final Thoughts & Recommendations

The January 2026 data confirms what we've been feeling on the ground: we are in a challenging, price-sensitive market.

For Sellers: You cannot look in the rearview mirror to price your home. With both sales and prices trending downward, you must price ahead of the market, not chase it down. Properly priced, well-presented homes are still selling, but buyers are refusing to overpay.

For Buyers: This is your moment. With less competition and prices pulling back, you have excellent negotiating power. Whether you are looking for a heavily discounted suburban semi or a starter condo, the opportunities are there if you are ready to act.

Want a personalized pricing strategy for your property?

Let’s chat and position your home ahead of the market, not behind it.